Fundraising Strategy for Beginners: A Confident, Practical Path to Your First Capital 🚀

Fundraising strategy for beginners can feel confusing at first, especially when every path seems to promise fast capital but comes with different risks, expectations, and tradeoffs. The good news is that you do not need to know everything to make a smart first move.

In this guide, you will learn how to choose the right fundraising path for your stage, avoid common beginner mistakes, and take practical steps toward your first real funding opportunity.

Why a fundraising strategy matters before your pitch deck

Most beginners start in the wrong place.

They open PowerPoint, Google Slides, or Canva and tell themselves the deck is the job. If the slides look polished enough, the thinking will somehow catch up later.

That is usually where the trouble starts.

A pitch deck is not a fundraising strategy. It is only a tool that presents one. If the strategy underneath is weak, the deck just hides the problem for a few more minutes. You may get a meeting, but once questions begin, the gaps show up fast.

Beginners often assume fundraising is mostly about persuasion. In reality, it is mostly about fit. You need the right amount, from the right kind of investor, at the right stage, for the right reason. If any of those four pieces are off, even a decent pitch can feel shaky.

That is why strategy has to come first.

Before you build slides, you should know what you are raising, why you are raising it now, and what that money is supposed to change in the business. Without those answers, you are not really fundraising yet. You are just asking people to fund uncertainty.

A deck cannot fix a fuzzy business decision

A lot of first-time founders quietly hope capital will solve confusion.

They are unsure about the customer, unsure about the offer, unsure about pricing, unsure about what the next six months should look like. So they decide to raise first and figure the rest out later.

From the founder side, that feels understandable. From the investor side, it looks risky.

Investors are not only asking, “Is this interesting?” They are also asking, “Does this founder know what this money is for?” If the answer sounds vague, confidence drops immediately.

That is why a strong fundraising strategy starts with a very boring question:

What exactly is the money meant to do?

For a beginner, that answer should be concrete. Not “grow faster.” Not “scale.” Not “expand the brand.” Those phrases sound ambitious, but they do not help anyone judge the raise.

A stronger answer looks more like this:

- finish product version two

- hire one technical lead

- move from pilot users to paying customers

- build a repeatable outbound process

- buy enough inventory to test real demand

- extend runway long enough to hit one important milestone

Notice what changed. The second version is measurable.

That matters because investors are not buying your excitement. They are buying a believable next step.

Strategy makes your pitch simpler, not more complicated

Founders often think strategy adds extra work. In practice, it removes wasted work.

When you are clear on the raise, the deck becomes easier to build because you stop trying to say everything. You know what matters. You know which proof points belong. You know which details are noise.

That also makes your pitch sound calmer.

Instead of performing, you start explaining.

Instead of saying, “We are changing the future of this category,” you say, “We have early proof in this niche, and this round is meant to help us turn that into a repeatable model.”

That second version is less dramatic, but much easier to trust.

And trust matters more than drama in a first raise.

What beginners should prepare before slide one

Before you touch your deck, put these answers into a short working document in Google Docs or Notion:

- How much are we raising?

- Why this amount and not less?

- What does the money fund over the next stage?

- What measurable result should it create?

- Why is now the right time to raise instead of waiting?

If you cannot answer those cleanly, the deck is still premature.

A quick example shows the difference.

A weak version sounds like this:

“We are raising $500,000 to grow the business.”

A stronger version sounds like this:

“We are raising $500,000 to finish onboarding automation, add one growth hire, and convert our pilot traction into 40 paying customers with retention data.”

The second version gives people something to evaluate. It feels grounded. It gives your raise shape.

That is the real job of early fundraising strategy. It turns a vague desire for capital into a specific business move.

The real danger of skipping strategy

The danger is not only rejection. It is wasted time.

When founders skip strategy, they usually do three costly things:

- talk to the wrong type of investor

- ask for an amount that does not match their stage

- build a story around aspiration instead of proof

Then they conclude fundraising is impossible, when the deeper problem was that the raise itself was not well designed.

That is why beginners should treat fundraising less like a presentation challenge and more like a business design challenge. The pitch deck comes later. First, you need to decide whether the raise makes sense, what kind of raise it is, and what “success” actually looks like.

Before moving to the next section, write your raise in one sentence: the amount, the purpose, and the milestone it should unlock.

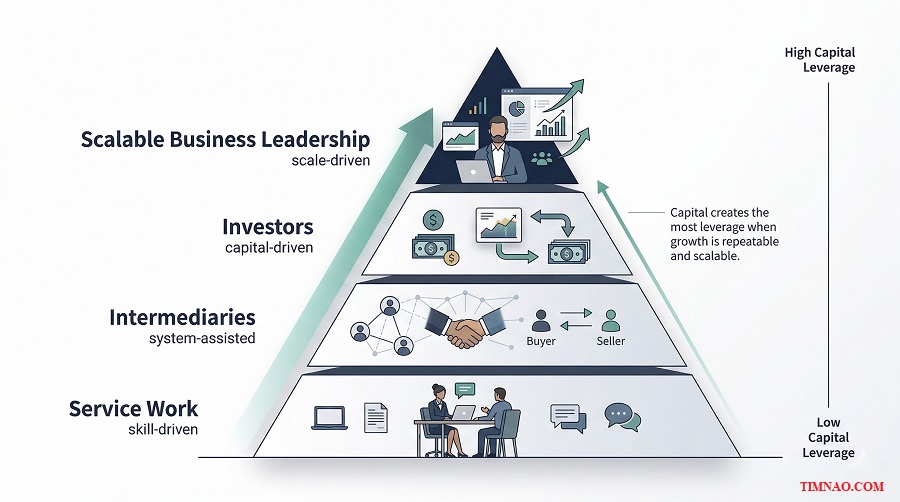

The wealth pyramid: choose the level where capital actually helps

One of the most useful mindset shifts for beginners is realizing that not every business benefits from outside capital in the same way.

This is where a lot of first raises go wrong.

A founder knows they are working hard, moving slowly, and feeling constrained. So naturally they think the answer must be money. But effort alone does not make a business a good fit for fundraising. What matters is whether capital creates leverage.

That is where the wealth pyramid becomes useful.

The basic idea is simple: capital behaves differently depending on where you sit in the economic structure. At some levels, extra money changes very little. At other levels, it can dramatically increase output.

The bottom layer: service work usually scales through skill, not capital

At the base of the pyramid is service work.

This includes freelancers, consultants, contractors, specialists, agency owners, and many professionals whose income rises as their skills become more valuable.

There is nothing wrong with that model. In fact, for many people it is the fastest way to build cash flow. The problem is that service work usually depends heavily on personal time, personal delivery, or a tightly managed team.

That means more money does not always create much more leverage.

If you give extra money to a solo consultant, they might buy better software, improve branding, or outsource some tasks. That can help. But it usually does not transform the economics overnight. The business still depends mostly on the founder’s direct effort.

That is why many service businesses are profitable but not especially fundable.

Investors are not asking whether the founder works hard. They are asking whether money changes the slope of the business.

The middle layer: systems start to matter more

As you move up, capital starts to matter more because repeatability begins to show up.

This is where intermediaries, brokers, marketplaces, distribution businesses, and more system-driven business models often live. These businesses do not rely only on one person’s craft. They rely on processes, networks, deal flow, or repeatable movement between buyers and sellers.

At this level, extra capital can be more powerful.

It can help you:

- build sales systems

- create stronger distribution

- fund customer acquisition

- improve tools that increase throughput

- expand reach without increasing direct labor at the same rate

This is the zone where many founders start to become more fundable, because the money does more than reduce stress. It increases capacity.

That is an important difference.

The top layer: capital is strongest when it turns into scale

At the highest level, capital becomes most effective.

This is where entrepreneurs and business leaders build something that can consume money and turn it into greater value. Product development, team building, infrastructure, distribution, brand growth, and market expansion can all accelerate if the model is working.

This does not mean every startup belongs here from day one.

It means this is the level where capital has the clearest compounding effect.

For example, if a founder already has signs of real demand, more capital can help them hire, build faster, close more customers, or expand a working system into a much larger one. In that case, money is not just helpful. It is catalytic.

That is what many beginners miss.

They assume investors back effort, ambition, or vision alone. Usually, investors back leverage. They want to see that capital placed into this business has a believable chance of producing more value than it would elsewhere.

A simple way to place your business honestly

If you want to know whether capital is likely to help right now, ask yourself these questions:

- Does revenue depend mostly on my personal delivery?

- Is the offer still heavily customized every time?

- Would more money create a repeatable growth engine, or just reduce pressure?

- Can I clearly explain how capital turns into more output?

- Is the next bottleneck really cash, or is it still clarity?

If your honest answers point to service-heavy economics, you may still build a great business. But the best next move may be to productize more, simplify more, or gather stronger proof before trying to raise outside money.

If your answers point to repeatability, leverage, and system-driven growth, fundraising may make more sense now.

A practical beginner example

Imagine two founders.

Founder A runs a profitable boutique branding studio. Clients love the work, but every project is custom, and the founder still leads most delivery. More money would help with nicer tools and maybe a contractor or two, but the business would still depend on the founder’s taste and time.

Founder B serves the same niche, but has turned one high-demand service into a productized offer, added templated workflows, delegated fulfillment, and built a repeatable sales process. More money would help expand capacity and acquire more of the right customers.

Both are smart. Both may be successful. But the second business is easier to finance because capital has somewhere clearer to go.

That is the point of the pyramid. It is not judging the value of the work. It is helping you see whether money is actually the right lever.

Before you chase investors, place your business on the pyramid as it exists today, not as you hope it will look a year from now.

Trust, demand, and attention: the investor test most beginners miss

Once you know whether capital can truly help, the next question becomes more human.

Why would anyone say yes?

Beginners often answer this with, “Because the idea is good.” But investors rarely make decisions that way. A good idea matters, of course, but money usually moves when three forces come together at the same time: demand, attention, and trust.

If one of them is weak, the whole process struggles.

Demand: does this solve something people actually care about?

Demand comes first because no amount of charisma can permanently rescue a weak market need.

For beginners, demand means more than “people said it was interesting.” It means there is a real problem, a real buyer, and a believable reason this solution matters now.

You should be able to explain:

- who has the problem

- how they solve it today

- why the current solution is frustrating, expensive, slow, or incomplete

- why your offer is meaningfully better

A founder saying, “We are building AI for health and wellness,” is not describing demand clearly.

A founder saying, “We help physical therapy clinics reduce no-shows with automated rebooking and reminder flows,” is getting much closer.

The second version points to a real pain point. It makes the need easier to picture.

That is what investors need. Not just a big category, but a believable reason this specific problem deserves attention.

Attention: can you make the opportunity easy to notice and remember?

Even a strong business can lose people if the story is dull, crowded, or too broad.

Attention is about earning the second minute, not just the first glance.

For beginners, attention usually comes from one of a few places:

- a sharp niche

- a timely market shift

- a surprisingly clear result

- a founder with unusual proximity to the problem

- early traction that makes the story harder to ignore

This is why specificity helps so much.

“We built software for service businesses” is easy to forget.

“We help med spas recover lost repeat bookings through automated follow-up” is much easier to remember.

Attention does not mean hype. It means the story lands quickly enough that someone wants to keep listening.

That is especially important in fundraising because investors are juggling many conversations. If your story takes too long to click, you lose momentum before trust even has a chance to build.

Trust: do you feel safe enough to bet on?

This is the piece beginners most often underestimate.

They think if demand is real and the product sounds exciting, the job is mostly done. But trust is what turns curiosity into actual movement.

Trust comes from signals like:

- founder honesty

- clear scope

- realistic claims

- follow-through

- relevant experience

- traction that matches the story

- calm answers under pressure

In simple terms, trust answers the question, “Would I feel comfortable giving this person money and waiting for results?”

That is not just about personality. It is about consistency.

If your business sounds different in every meeting, trust goes down. If you exaggerate traction, trust goes down. If your ask is fuzzy, trust goes down. If you cannot explain what the money is for, trust goes down.

On the other hand, small proof points can build trust surprisingly fast.

A founder who clearly understands the customer, has a focused plan, and speaks honestly about what is still unproven often feels safer than someone with a bigger vision and a more inflated story.

The investor test in real life

A simple way to use this framework is to write one sentence for each element.

Demand: what painful problem exists, for whom, and why now?

Attention: what makes this opportunity worth noticing fast?

Trust: why are we believable people to execute this next step?

Here is a basic example.

Demand: Independent gym owners lose recurring revenue because follow-up after trials is inconsistent.

Attention: Our tool plugs into the systems they already use and automates that gap.

Trust: We ran operations in gyms for years and already have early pilot usage.

That story is not flashy. But it gives an investor something solid to react to.

And that is what many first-time founders need most. Not a bigger pitch. A cleaner one.

Before you move on, write your own three-line version for demand, attention, and trust. If one line feels weak or vague, that is probably the real fundraising problem to fix next.

The law of differentiation: make your story easier to buy

By the time a founder starts talking to investors, one question is always sitting quietly in the room: why this company, and why now?

That is where differentiation matters. But beginners often make it much harder than it needs to be.

They assume differentiation means sounding disruptive, futuristic, or impossible to copy. So the pitch gets loaded with big language, broad claims, and too many moving parts. The result is a story that sounds ambitious but feels slippery.

In practice, good differentiation does something much simpler. It makes your business easier to understand, easier to remember, and easier to believe in.

Differentiation is not about sounding bigger

A lot of first-time founders think they need to sound like a massive company before they have earned the right to. That usually backfires.

If your business is still early, the goal is not to sound enormous. The goal is to sound clear enough that someone can quickly understand where the edge comes from.

That edge might come from:

- a customer group you understand unusually well

- a painful problem you can solve faster than others

- a simpler delivery model

- a sharper niche

- a better distribution angle

- early proof that the market is already responding

None of that requires hype.

For example, compare these two lines:

“We are building an AI-powered ecosystem for service-business growth.”

“We help independent clinics reduce missed follow-ups and recover more repeat bookings.”

The first line sounds broader. The second line is easier to buy because people can picture the problem and the outcome without doing mental gymnastics.

That is the real test. If your story needs too much translation, differentiation is getting buried under language.

Your story becomes stronger when it answers one practical question

A useful way to tighten your positioning is to ask:

What makes this business easier to bet on than the obvious alternatives?

For a beginner, that usually comes down to three things.

You know the customer better than outsiders do

This is one of the most underrated forms of differentiation.

You may not have the biggest product yet. You may not have the most funding. But if you deeply understand the customer’s workflow, frustrations, and buying logic, your offer often lands faster.

That is why founder-market fit matters. It gives your story weight.

A former recruiter building software for recruiting teams has a more believable starting point than someone who picked the category because it looks large on paper. A creator building tools for creators has an easier time spotting what really wastes time and what looks useful but is not.

For beginners, lived proximity is often a stronger differentiator than clever branding.

Your offer creates a clear result, not just a feature list

Founders love features because they feel tangible. Investors and customers care more about outcomes.

If your explanation sounds like a stack of functions, people work harder to understand why the business matters. If your explanation points to a specific result, the story becomes easier to hold onto.

Instead of saying:

- dashboard

- automation

- AI assistance

- reporting

- integrations

Try saying what changes for the buyer:

- less manual work

- fewer missed follow-ups

- faster onboarding

- more repeat bookings

- better response time

This is especially important in fundraising because investors are constantly comparing opportunities in their head. The clearer the result, the easier the comparison.

Your business is narrow enough to feel real

Beginners often think narrowing the story makes the opportunity smaller. Usually it does the opposite.

When you narrow the story, it becomes more believable.

“We serve healthcare providers” is broad.

“We help private physical therapy clinics fill schedule gaps caused by late cancellations” is far more concrete.

The second version gives people something they can trust. It also opens the door to more useful questions about the buyer, pricing, retention, and rollout.

That is what you want. Not vague admiration. Useful engagement.

Make the story easy to repeat after the meeting

A good fundraising story does not only work while you are in the room. It keeps working after the meeting ends.

That matters because investors often need to repeat your idea internally, compare it with other companies, or explain it to partners. If your story is hard to retell, it becomes harder to support.

This is why simple stories travel further.

A practical way to test this is to write your company in three short lines:

- Who is it for?

- What painful problem does it solve?

- Why is your version the one worth paying attention to?

If the answer becomes a paragraph, it is still too tangled.

A beginner-friendly example might look like this:

We help independent dentists reduce front-desk admin.

Our software automates reminders, rebooking, and patient follow-up.

We know the workflow well, and early clinics are already using it to save staff time.

That is not flashy. It is usable.

What usually weakens differentiation

If your pitch feels muddy, it is often because one of these habits has crept in:

- trying to serve too many markets at once

- mixing multiple products into one story

- leading with technology instead of the customer problem

- using abstract language instead of practical outcomes

- making the opportunity sound bigger than the current proof supports

Founders do this because they want to appear ambitious. But investors do not usually reward inflation. They reward clarity tied to believable upside.

Before moving on, rewrite your company story in plain English and read it out loud. If it sounds like a startup slogan instead of a real business, simplify it again.

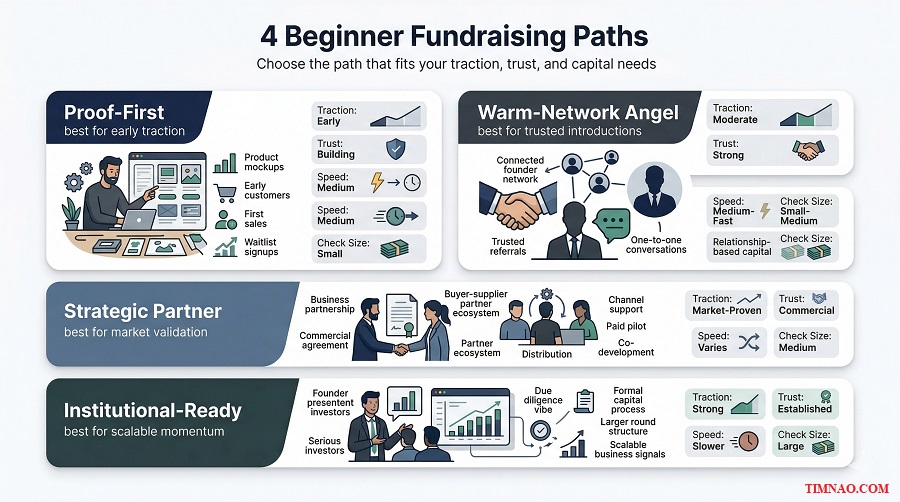

Four beginner fundraising paths that fit different constraints

Once the story is clearer, the next decision is not how to pitch harder. It is how to choose the route that actually matches your stage.

This is where many beginners lose momentum. They mix together several fundraising styles at once, then wonder why the process feels messy. They talk to angels, chase funds, hope for strategic partners, and consider bootstrapping all in the same month.

The result is usually confusion, not progress.

A cleaner approach is to choose one primary path based on your constraints: time, proof, network, and how much risk still sits inside the business.

Path 1: build proof before you chase a real round

This is often the smartest path for founders who are still early.

If the business has promise but limited proof, your first job is not to sell the full vision. It is to collect signals that make the next raise easier.

That proof could look like:

- first paying customers

- a working pilot

- pre-orders

- a strong waitlist with real intent

- repeat usage

- better margins than expected

- a conversion pattern that shows people actually want this

This path often includes self-funding, client-funded development, revenue from services, a small friends-and-supporters round, or a grant that buys time to hit a milestone.

What makes this route strong is that it lowers future friction. Instead of asking investors to believe mainly in your idea, you start giving them something they can inspect.

For beginners, this is often the difference between a hard sell and a much easier next conversation.

Path 2: raise from warm angels who can understand you quickly

This path works best when you already have some traction and some trust around you.

Warm angels do not need to be celebrities or famous startup names. They might be operators, niche founders, experienced professionals, or people in your network who understand the market well enough to evaluate you quickly.

This route fits founders who have:

- relevant industry experience

- introductions through customers, peers, or advisors

- early traction that is easy to explain

- a round size that can realistically be assembled from several smaller checks

The strength of this path is speed with context. You spend less time explaining the basics because the investor already has some lens for the category or for you.

The tradeoff is that small checks often mean you need multiple yeses, and those conversations require more coordination than beginners expect.

Still, if your story is clear and your ask is realistic, this route can be much more practical than trying to force institutional attention too early.

Path 3: let strategic partners validate the business first

Some founders ignore this option because it does not look like classic fundraising.

That is a mistake.

In many early businesses, the most valuable source of capital is not a traditional investor. It is a customer, distributor, supplier, or industry partner who directly benefits if your business works.

That support may not always come as equity. It can come through:

- prepayment

- paid pilots

- co-development

- guaranteed volume

- revenue commitments

- access to distribution

- commercial partnerships that remove early risk

This path is especially useful when your business solves a painful operational problem for a specific type of buyer.

Why does it matter so much?

Because commercial proof often carries more weight than a polished pitch. A paying partner tells the market that the problem is real and the solution is useful. That can make future fundraising much easier.

The tradeoff is that these deals need care. A bad strategic arrangement can narrow your freedom or create dependency too early. But if structured well, this path can be one of the strongest bridges between early demand and later capital.

Path 4: go after institutional capital when the business can absorb it well

This is the path many founders fantasize about first, but it only works well when the business is ready for it.

Institutional investors usually need more than a promising idea. They want clearer evidence that the company can absorb capital and turn it into meaningful progress.

That usually means:

- stronger traction

- a more disciplined story

- better understanding of unit economics or growth logic

- a larger market case

- cleaner use of funds

- a process that can withstand real diligence

This path makes sense when capital is not just helpful but catalytic. In other words, when more money can clearly accelerate something that is already beginning to work.

Beginners often reach for this path too soon because it looks like the most “startup” option. But if the business still needs basic proof, this route becomes a long series of polite conversations that go nowhere.

A simple rule helps here: if the company still needs belief more than evidence, it is probably not time for institutional outreach yet.

How to choose without spinning in circles

If you are unsure which path fits, use the constraint test:

- If you need evidence more than exposure, choose the proof-first path.

- If you have traction and credible introductions, choose the warm-angel path.

- If industry players benefit directly from your success, explore the strategic-partner path.

- If the business already shows real momentum and capital can clearly amplify it, the institutional path may make sense.

You can move from one path to another over time. What hurts beginners is not choosing imperfectly. It is trying to run all four paths at once.

At this stage, pick one primary lane and let your actions match it for the next month.

Money in motion: build a realistic investor list instead of a fantasy one

Once you know your path, the next temptation is to build an investor list that looks impressive.

That is where many founders drift back into wishful thinking.

They fill a spreadsheet in Google Sheets or Airtable with famous funds, recognizable angels, and people they admire online. The list becomes long, but not useful.

A realistic investor list works differently. It starts with movement, not status.

The right investor is not the most famous one

Beginners often confuse prestige with fit.

A big brand name may look exciting, but if that investor writes larger checks, invests later, avoids your category, or rarely backs businesses like yours, they are not part of your real pipeline. They are just a familiar logo.

The better question is:

Whose money is already moving toward companies like mine?

That one shift changes everything.

If you are building a niche B2B tool with early traction, the best targets may be specialist angels, operators, or early-stage funds that already understand the workflow you are improving. If you are productizing a business in a narrow vertical, someone who knows the niche may be far more valuable than a famous generalist.

Money moves more easily when it is already flowing in roughly your direction.

What a practical investor list should filter for

A useful list is usually smaller and sharper than beginners expect.

Before adding a name, check for:

- stage fit

- sector fit

- likely check size

- geography fit

- decision speed

- realistic path to access

If the fit is weak on most of those points, the name probably should not be in your active list.

This is not about being pessimistic. It is about protecting your time.

A founder with 20 well-qualified names often has a better starting point than a founder with 120 weak ones. The second list feels bigger, but the first one usually creates better momentum.

Why fantasy lists are so common

They show up for predictable reasons.

First, famous names create emotional comfort. It feels like progress to add recognizable investors, even when the match is poor.

Second, beginners often build lists around admiration instead of buying behavior. They know who sounds smart online, but not who actually writes checks into businesses at their stage.

Third, a long list creates the illusion of safety. It feels like a pipeline, even when most names have almost no chance of converting.

That is why realistic list-building is less glamorous and far more useful.

Start with people who need less convincing

A good early investor list usually includes people who already understand at least one part of your world.

That might be:

- operators turned angels

- founders investing in adjacent categories

- small funds active in your stage

- niche investors with sector familiarity

- strategic players close to the market

- trusted contacts introduced through customers or advisors

These people are valuable because they do not need a 20-minute lesson just to understand why the business matters. Their money, attention, or pattern recognition is already closer to your direction.

That shortens the gap between curiosity and conviction.

A beginner-friendly way to build your first real list

Instead of one giant spreadsheet, build your list in three tiers.

Tier 1: high fit, reachable now

These are the people you would contact first. Strong stage fit, strong category logic, and at least some believable path to a conversation.

Tier 2: high fit, but colder

These names still make sense, but access is weaker. They are worth working toward after you tighten your first wave.

Tier 3: selective stretch names

A few aspirational targets are fine, as long as there is still logic behind them. The mistake is turning the whole list into Tier 3.

This tiered method keeps the process grounded. It also prevents the common beginner habit of spending too much energy on low-probability names while ignoring reachable ones.

Before you finish this section, build a first-pass list of 25 names and sort them into the three tiers. If a name is there only because it looks impressive, remove it.

Pipeline, conversion rate, and bite size: do the math before outreach

By this stage, the story should be clearer. You should know what kind of raise you are trying to make, what kind of investor fits it, and what the money is supposed to unlock.

Now comes the part many beginners avoid because it feels less exciting than pitching: the math.

That is a mistake.

A lot of first raises become stressful not because the founder is bad at fundraising, but because the raise was never translated into workable numbers. The founder knows how much money they want, but not how many serious conversations they likely need, how big the typical check might be, or how wide the pipeline has to be for the round to close without panic.

Once you do that math, fundraising becomes easier to manage. It may still be hard, but it stops feeling random.

Pipeline means qualified opportunities, not a long contact list

Many founders say they have a pipeline when what they really have is a spreadsheet full of names.

That is not the same thing.

A real fundraising pipeline is a group of people who could realistically invest in your company at this stage, in this round, and within a time frame that still matters. If a name looks impressive but the person rarely invests in your category, prefers later-stage companies, or usually writes checks far above or below your range, that person is not really in your pipeline.

They are just on your list.

This distinction matters because beginners often overestimate how many real shots they have. A spreadsheet might contain 70 names, but once you filter for fit, actual access, and likely interest, maybe only 20 to 30 are truly live options.

That is normal. It is also useful to know early.

A practical pipeline usually includes:

- people who invest at your stage

- people who understand your kind of business

- people who can write checks in a range that helps

- people you can realistically reach, either directly or through an introduction

- people who can move within a timeline that matches your runway

That is already enough to work with. You do not need a giant list. You need a believable one.

Conversion rate tells you where the raise is actually breaking

Most beginners think conversion means one thing: someone said yes or no.

In reality, fundraising conversion happens in stages.

If you do not break those stages apart, it becomes hard to tell whether the real problem is your outreach, your story, your investor fit, or your ask.

A simple version looks like this:

- Outreach to first meeting

- First meeting to second meeting

- Second meeting to deeper diligence

- Diligence to verbal commitment

- Verbal commitment to money actually wired

Each step tells you something different.

If almost nobody responds to outreach, the issue may be investor fit, cold messaging, or weak introductions. If first meetings happen but rarely turn into second meetings, the story may not be landing. If second meetings happen but commitments do not follow, the problem may sit in trust, traction, or round design.

That is why vague impressions can mislead you.

Founders often say things like:

- “People seem interested.”

- “The calls are going well.”

- “We’re getting decent feedback.”

That may all be true, but unless the process is moving forward, you still need to know where it is slowing down.

A founder who understands their conversion pattern can improve much faster than one who is only reacting emotionally from meeting to meeting.

Bite size has to match the actual market around you

Bite size is the realistic check size you can expect from the kind of investors you are targeting.

This is where a lot of first-time founders quietly sabotage themselves.

They decide how much they want to raise, divide it by a comfortable number, and assume that each investor will naturally fill that role. But fundraising rarely works like that. Your preferred average check size and the market’s realistic average check size are often not the same.

For example, if you are most likely to raise from angels who typically write small to mid-sized checks, but your plan only works if each person contributes much more, your round becomes fragile. You either need more investors, a smaller target, or a different capital mix.

This is why honest bite-size thinking matters so much.

Your likely average check depends on:

- your stage

- your traction

- the type of investor

- how risky the opportunity still feels

- the amount you are raising relative to the market around you

Beginners often make life harder by copying round sizes from startup stories they have read online. But your round does not need to look like someone else’s. It needs to close.

A simple example that makes the math real

Let’s say you want to raise $250,000.

You believe the most likely investors in your current network can write around $25,000 each. That means you need roughly 10 solid commitments.

Now imagine your actual conversion from serious investor conversation to commitment ends up around 20%.

That means you do not need 10 serious conversations. You need about 50.

And to get 50 serious conversations, you may need a larger top-of-funnel number depending on how warm your outreach is. If most of your process is warm introductions, the early-stage conversion may be better. If most of it is cold, you may need many more names to produce the same number of good meetings.

This is why founders should do the math before outreach, not after three weeks of frustration.

When the numbers are visible, you can ask much better questions:

- Is my pipeline wide enough?

- Is my average expected check too optimistic?

- Am I trying to close too much money too quickly?

- Do I actually need more investor names, or do I need a better second meeting?

That is a much healthier place to operate from.

Round design matters more than motivation

A lot of beginner pain in fundraising comes from treating the raise as a motivation problem.

The founder thinks, “I just need to pitch harder, send more emails, or stay more confident.”

Sometimes effort does matter. But often the deeper issue is round design.

You may be asking for too much relative to your traction. You may be targeting investors whose typical check size creates unnecessary pressure. You may be trying to close a full round when a smaller bridge would be more realistic. You may be moving too slowly for your runway, or too fast for the kind of people you are approaching.

These are not mindset problems. They are design problems.

And design problems can be fixed.

For example:

- a founder who needs money quickly may reduce the round and prioritize warm angels first

- a founder with strong demand signals but limited investor access may start with a commercial partner

- a founder with too few likely investors may split the raise into two stages

- a founder whose likely buyers write smaller checks may widen the pipeline before expecting momentum

That is what practical fundraising looks like. Not just staying positive, but adjusting the structure until the numbers make sense.

A simple system for tracking without overcomplicating it

You do not need a fancy CRM to run a first raise well.

A clean tracker in Google Sheets, Airtable, or Notion is usually enough. What matters is that you update it honestly.

At minimum, track:

- investor name

- stage and sector fit

- likely check range

- warm, semi-warm, or cold

- first contact date

- latest status

- key objection or hesitation

- next step

- next follow-up date

This is not busywork. It helps you spot patterns before they become expensive.

If several investors like the market but hesitate on your traction, that tells you something. If interest is strong but timelines are too slow, that tells you something too. Good tracking makes the raise feel less like guesswork and more like a process you can steer.

Before moving on, write down three numbers: your target raise, your realistic average check, and the approximate number of serious conversations you probably need. Those three numbers will shape the rest of your outreach.

Your 30-day fundraising roadmap at two speeds

Once the math is clear, the next step is not to “go raise.” That is too vague.

What helps beginners most is a short runway with clear priorities. A 30-day plan works well because it is long enough to build momentum and short enough to stay real.

The key is to choose a speed that matches your actual life. Some founders can work on fundraising almost every day. Others are juggling client work, product work, or a day job. Both situations are workable, but only if the plan is honest.

Track A: the steady daily pace for founders actively raising now

This track works best if you can protect around 45 to 60 minutes a day, five or six days a week.

It is a strong fit if:

- you already know you are raising now

- the business has some proof

- your runway or market timing makes this month important

- you can stay consistent without dropping the rest of the business

The value of this track is momentum. Small daily progress compounds quickly in fundraising.

Week 1: get the raise clear enough to explain in one breath

The first week is not about outreach. It is about clarity.

By the end of the week, you should be able to explain:

- how much you are raising

- why this amount makes sense

- what the money will fund

- what milestone it should unlock

- what kind of investor is the best fit

This is also the right moment to clean up the core story. Your goal is not to sound grand. Your goal is to sound coherent.

A useful test is this: could you explain the raise clearly without opening a deck?

If the answer is no, that is still the work.

For many beginners, week one is where the raise becomes real for the first time. Up to that point, it is often just a wish with a number attached to it.

Week 2: build the investor list you can actually work

Now that the raise is clearer, you can build the active list.

Do not try to find everyone. Try to find the right people.

Split the list into:

- warm targets

- high-fit but colder targets

- stretch targets worth keeping on the edge of the process

Rank them by fit, not by reputation.

This week is also where you map access. For each high-priority name, ask:

- do I know them directly?

- who could introduce me?

- what is the cleanest way in?

- if I reach out cold, what is the strongest angle?

A beginner mistake is treating all names equally. They are not. Some conversations are worth far more because they can create introductions, social proof, or momentum even if they do not invest themselves.

Week 3: prepare the materials people actually need

This is where the deck belongs.

Not before strategy. Not before the list. Here.

By now you know what the raise is, who it is for, and what questions are likely to come up. That makes the materials much easier to shape.

For most first raises, you need:

- a concise deck

- a short written summary

- a clear founder bio

- basic traction or proof points

- simple answers to likely objections

This is also the week to pressure-test your story. Talk through it with one person who understands business and one person who does not. If both can follow it, you are in a better place.

You do not need to impress everyone with polish. You need materials that support confidence.

Week 4: begin outreach and treat the first meetings as data

This is the week many founders wait too long to begin.

Once week four starts, your job is to move. Not recklessly, but deliberately.

Start with the highest-fit conversations first. Warm intros usually deserve priority, especially in a first raise. Your early meetings are not just about closing capital. They are also about pressure-testing the story in the real world.

Pay attention to:

- which lines create interest

- where people get confused

- what questions repeat

- where momentum increases

- what causes the conversation to cool

That information is gold. It helps you improve while the raise is still young.

A first month of fundraising does not need to end with a closed round. It needs to end with a stronger process than the one you started with.

Track B: the lighter weekly pace for busy founders and side-builders

Not every founder can or should run the daily version.

If you are still working full-time, managing clients, or building in the margins of a packed week, a lighter pace is often more realistic. That does not make it weak. It just means the process needs more discipline and less drama.

This track works well if you can give two or three focused sessions a week.

Week 1: define the raise without turning it into a side hobby

Your goal this week is not to “think about fundraising.” It is to define it.

Use your sessions to lock in the basics:

- target amount

- use of funds

- next milestone

- best-fit investor path

If you end the week with cleaner thinking, you are on track. If you end the week with more tabs open and no real decisions made, simplify.

A focused founder with limited time usually beats a scattered founder with more hours.

Week 2: build a shortlist, not a fantasy pipeline

This week is about making the process manageable.

Instead of trying to build a giant investor database, create a shortlist you can actually move on. Fifteen to twenty well-chosen names can be enough to start, especially if some are warm.

Use one session for warm contacts, one for higher-fit cold or semi-warm names, and one to sort them by priority.

This lighter pace works because it forces judgment. You cannot afford a bloated list, so the quality has to be better.

Week 3: prepare lean materials you can use confidently

At a slower pace, simple materials matter even more.

A deck that is too long becomes harder to maintain. A story that is too broad becomes harder to carry between busy weeks.

Keep it lean:

- a short deck

- a short written summary

- a short explanation of what the round changes

That may sound basic, but most beginner fundraising gets stronger when the materials get shorter.

Week 4: start the process without waiting to feel “fully ready”

A lot of founders using the slower track delay outreach because they feel they have not had enough time to perfect the process.

That is usually a trap.

At some point, the process has to meet reality. Send the first emails. Ask for the first introductions. Take the first conversations. Then tighten based on what comes back.

If your week is crowded, it is better to send five strong messages and follow them properly than to draft 30 and ghost the follow-up.

That is the main principle of the slower track: lower volume, higher intentionality.

Whether you choose Track A or Track B, put the fundraising sessions on your calendar now. If they are not scheduled, they usually lose to everything else.

Signals that tell you to stay the course, tighten the story, or pivot

Once the process starts, it becomes easy to overreact.

A polite rejection can feel like a disaster. One enthusiastic meeting can feel like the round is suddenly inevitable. Neither reaction is especially helpful.

What helps is reading the process through signals.

Signals tell you whether the current approach is working, whether the story needs tightening, or whether the path itself is off.

Stay the course when the quality of the conversations is improving

Not all healthy fundraising looks dramatic.

A process can be working even when no money has landed yet. The key question is whether the quality of engagement is moving in the right direction.

Good signals include:

- people understand the business quickly

- second meetings are happening

- follow-up questions get more specific

- introductions increase after conversations

- investors start discussing terms, timing, or structure

- objections become narrower instead of broader

These signs show that the core story is landing and the process is getting warmer.

Beginners often expect momentum to feel obvious. More often, it shows up quietly through better questions, faster replies, and deeper conversations.

Tighten the story when interest keeps stopping at the surface

Sometimes investors are friendly, responsive, even curious, but nothing really moves.

That usually means you have enough attention to earn a meeting, but not enough clarity or trust to keep the process moving.

Common signs include:

- people say the space is interesting, but nothing deepens

- the same basic confusion appears in multiple meetings

- investors ask what you do in slightly different ways because the story is not sticking

- your explanation changes too much depending on who you are talking to

- you keep hearing “a bit early” without clear next steps

When this happens, the answer is rarely “talk to more people immediately.” Usually the better move is to tighten the message.

That may mean:

- narrowing the customer

- simplifying the offer

- making the use of funds more concrete

- showing stronger founder-market fit

- replacing broad claims with one believable next milestone

A tighter story does not have to be louder. It just has to reduce friction.

Pivot the path when the mismatch is structural

Sometimes the issue is not wording. It is the route.

If the pattern keeps pointing to the same deeper problem, you may need to pivot the path instead of polishing the same pitch.

That is usually true when:

- the likely checks are too small for the round you are forcing

- strategic buyers care more than investors do

- investors repeatedly point to missing proof, not missing storytelling

- your timeline is too urgent for the kind of capital you are chasing

- your business still behaves more like customized service work than scalable product

- the best-fit people all hesitate for the same structural reason

In that case, the smartest move may be to:

- reduce the raise

- split it into stages

- shift from institutions to angels

- focus on commercial validation first

- spend 60 to 90 days collecting stronger proof before pushing again

That is not failure. It is course correction.

Consistency is one of your strongest trust signals

Founders often focus on charisma and overlook consistency.

But consistency is what makes people feel safe.

If your numbers shift casually from one meeting to the next, trust drops. If you promise quick follow-up and disappear for a week, trust drops. If your explanation of the market keeps changing, trust drops. If you sound calm one day and desperate the next, people notice that too.

This does not mean you need to sound polished in a fake way. It means you need to sound stable.

Reliability is persuasive because it lowers perceived risk. And for a first-time founder, that matters a lot.

Review the process before emotion takes over

A simple post-meeting review can help you stay objective.

After each conversation, write down:

- What seemed to resonate most?

- Where did the person hesitate?

- Was the issue fit, traction, trust, timing, or check size?

- Did the conversation clearly move forward?

- What, if anything, should change before the next one?

Do this consistently and the noise starts to become pattern.

After eight to ten meetings, you will usually know much more than you did at the start. You will see whether the round is basically healthy, whether the story needs tightening, or whether the path itself needs to change.

That is how experienced founders get calmer during a raise. Not because the process is easy, but because they read it more clearly.

Key takeaways for your first raise

- Do the math before outreach so you know whether your real constraint is pipeline, conversion, or average check size.

- Build a raise that fits your current stage, not the startup image you think you are supposed to project.

- Choose a 30-day pace you can actually maintain, then protect that time like it matters.

- Treat early meetings as feedback loops, not just chances to get a yes.

- Tighten the story when interest stays shallow, and change the path when the mismatch is deeper than messaging.

- Let consistency do some of the persuasion for you. In a first raise, reliability often matters more than performance.

Disclaimer:

This article is for educational and informational purposes only and should not be considered legal, financial, tax, investment, or fundraising advice. Every business, fundraising path, and investor situation is different, so readers should do their own research and speak with qualified professional advisors before making financial or strategic decisions. Any examples in this article are for illustration only and do not guarantee fundraising success or specific results.

Enjoyed this article and found it helpful? ☕✨

You can support my work and help me create more practical, beginner-friendly guides here: Buy Me a Coffee 💛

{kind=link}