Rational Long-Term Investing: A Calm Power Plan for Beginners 🚀

Rational long-term investing sounds boring until a “hot stock” turns red and you realize you never had a real plan. For beginners, the smartest path is not chasing every market trend, but building a simple system that protects your cash, grows your money steadily, and keeps emotions from making expensive decisions.

This guide shows you how to move from random investing to a calmer wealth-building plan: clear your financial foundation, use passive ETFs wisely, research individual stocks with better filters, and create rules you can actually follow when the market gets noisy.

The Costly Moment a Hot Stock Stops Feeling Smart

Maya did not think she was gambling.

She thought she was finally “doing something smart” with her money.

A finance creator she followed had posted a video about a stock that was “still early.” The company sounded exciting. The chart looked strong. The comments were full of people saying they were buying more before “Wall Street noticed.”

So Maya opened her investing app during lunch and bought $1,200 worth of shares.

At first, it felt amazing. The stock went up a little. Her account turned green. She refreshed the app between meetings and imagined what would happen if it doubled.

Then the company released disappointing news.

The stock dropped. Then dropped again.

Her $1,200 became $940. Then $810. Then $760.

The worst part was not just the money she lost. It was the feeling that she had no idea what to do next.

Should she sell? Buy more? Wait? Was this a temporary dip or a sign the business was in real trouble?

That is the moment a hot stock stops feeling smart.

It is also the moment many beginners realize they did not buy an investment. They bought excitement.

A stock tip is not an investing strategy

A stock tip can feel useful because it gives you a clear action: “Buy this.”

But it does not give you a system.

It usually does not tell you:

- Why the business is valuable

- What could go wrong

- How much the company is actually worth

- When the investment becomes too risky

- What to do if the price falls 30%, 50%, or more

That missing information matters.

When you buy based on hype, you are depending on other people’s confidence. The moment the price falls, that borrowed confidence disappears.

A real investing strategy gives you something stronger: your own reasoning.

You know why you bought. You know what you are watching. You know what would make you hold, buy more, or sell.

That does not mean you will always be right. No investor is always right. But it does mean you are making decisions from a plan instead of panic.

The market rewards ownership, not excitement

One of the biggest mindset shifts for beginners is this:

A stock is not just a moving price on a screen. It is a small ownership stake in a real business.

When you buy shares, you are buying into the future earnings, decisions, products, customers, and risks of that company.

That is very different from buying because the chart looks exciting.

For example, imagine two people buy the same stock.

The first person buys because a creator said it might “explode soon.”

The second person buys because they understand the business, believe it has a strong advantage, trust the management, and think the stock is selling for less than the business is worth.

Same stock. Totally different behavior.

If the price falls, the first person feels lost. The second person goes back to the original reasoning and asks, “Has the business changed, or has only the price changed?”

That question is powerful.

It separates investors from speculators.

The beginner mistake is not being wrong. It is being unprepared.

Maya’s mistake was not that she picked a stock that went down.

Even great investors buy stocks that fall after they buy them. Short-term price drops are normal.

Her real mistake was that she entered the market without preparation.

She had no emergency fund. She still had credit card debt. She had no monthly investing plan. And she did not understand the business well enough to judge whether the price drop was an opportunity or a warning sign.

That combination is dangerous.

A beginner can survive a bad stock pick if the position is small and the rest of their financial life is stable. But if someone invests money they may need soon, carries expensive debt, and reacts emotionally to every price move, even a normal market dip can become painful.

This is why rational investing starts before stock picking.

Before you ask, “What should I buy?”

Ask:

- Am I financially stable enough to invest?

- Can I leave this money alone for years?

- Do I have a plan if the market falls?

- Am I investing to build wealth, or just chasing a quick win?

These questions are not as exciting as a hot stock video.

But they are the questions that protect your money.

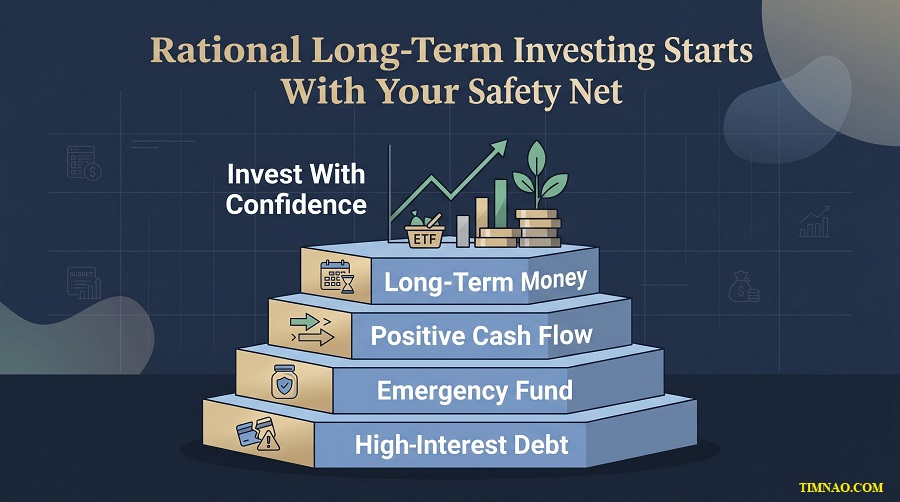

Rational Long-Term Investing Starts With Your Safety Net

The most underrated investing tool is not an app, chart, or stock screener.

It is a safety net.

That may sound boring, but boring is exactly what you want your foundation to be.

If your financial life is fragile, the market becomes more stressful than it needs to be. You might own a good investment, but if rent is due, your car breaks down, or your income suddenly drops, you may be forced to sell at the worst possible time.

That is how temporary market volatility turns into a real loss.

Rational long-term investing means building your life so you are not forced into bad decisions.

Pay down high-interest debt before chasing market returns

High-interest debt is like running a race with a backpack full of bricks.

You can still move forward, but everything is harder.

Credit cards, payday loans, and expensive personal loans can quietly destroy wealth because the interest keeps growing while you are trying to invest.

Here is a simple example.

Suppose you have $1,000 in credit card debt with a very high interest rate. You also have $1,000 cash available.

You could invest that money and hope for a good return.

Or you could pay off the debt and stop the interest from growing.

For most beginners, paying off expensive debt first is the cleaner move. It gives you a guaranteed improvement: you remove a cost that was dragging you backward.

This is not about being afraid of investing. It is about doing things in the right order.

A practical rule:

If the debt interest rate is high enough that it would be difficult to reliably beat through investing, prioritize the debt.

This gives you more breathing room. And breathing room is what allows you to invest calmly later.

Build an emergency fund so life does not raid your portfolio

An emergency fund is money set aside for real surprises.

Not vacations. Not shopping. Not “I saw a good deal.”

Real emergencies.

Think:

- Job loss

- Medical expenses

- Urgent home repairs

- Car repairs

- Family emergencies

- Pet emergencies

Without this buffer, your investment account becomes your emergency fund. That is risky because the market does not care when you need cash.

You might need money during a downturn.

If your portfolio is down 25% and you are forced to sell, that loss becomes permanent. If you had cash available, you could leave your investments alone and give them time to recover.

For many beginners, a good target is three to six months of essential expenses.

If your income is stable, three months may be a reasonable starting point. If your income is irregular, you support family members, or your job situation is uncertain, six months may feel safer.

Do not overcomplicate this.

Start with one month of essential expenses. Then build from there.

The first measurable win is not having a perfect emergency fund. It is reaching the point where a surprise bill no longer pushes you into panic.

Know your personal profit and loss

Every business needs to know whether it is making or losing money.

So do you.

Your personal profit and loss is simply:

Money coming in minus money going out.

If the number is positive, you have fuel for saving, investing, and debt repayment.

If the number is zero or negative, investing becomes much harder because you are trying to build wealth without extra cash.

To calculate it, review your last three months of spending.

Group your expenses into simple categories:

- Housing

- Food

- Transport

- Utilities

- Debt payments

- Subscriptions

- Insurance

- Family support

- Fun spending

- Savings and investing

Then ask two questions.

First: “Where is money leaking without improving my life?”

Second: “What monthly amount can I invest without needing it back soon?”

That second question is important.

Do not choose an investing amount that looks impressive but stresses you out. Choose an amount you can repeat.

A beginner who invests $100 every month for years is building a stronger habit than someone who invests $2,000 once, then stops because life gets tight.

Consistency is the asset.

Your time horizon decides how much risk you can handle

Money you need soon should not be treated the same as money for the next 20 years.

If you need cash for rent, taxes, tuition, a home deposit, or a major purchase within the next few years, that money should usually stay safer and more accessible.

Long-term investing works best with money that has time.

Time gives your investments room to survive recessions, market drops, bad headlines, and emotional cycles.

This is why beginners should separate money into buckets:

- Daily money — bills and normal spending

- Safety money — emergency fund

- Short-term goal money — planned expenses in the next few years

- Long-term money — investing for future wealth

Only the fourth bucket belongs in the market.

This simple separation prevents many bad decisions.

It also makes investing less scary because you know your life does not depend on tomorrow’s stock price.

Passive Investing and ETFs Build the Base Before You Chase Upside

Once your safety net is in place, the next question is simple:

What should your first real investing habit look like?

For most beginners, the answer is not individual stock picking.

It is a passive investing base.

Passive investing means you are not trying to guess which company will win next month. Instead, you invest in a broad group of companies through funds such as index funds or ETFs.

An ETF, or exchange-traded fund, is a fund you can buy and sell on the stock market. Many ETFs hold a basket of assets, such as hundreds of stocks.

For example, an ETF tracking the S&P 500 gives investors exposure to many large U.S. companies through one investment.

That does not remove all risk. The market can still fall.

But it removes the pressure of needing to find the single perfect stock as a beginner.

A broad ETF reduces single-company risk

When you buy one company, your result depends heavily on that company.

If management makes poor decisions, competitors become stronger, demand falls, or the business takes on too much debt, your investment can suffer badly.

A broad ETF spreads your money across many companies.

Some will disappoint. Some will perform well. Some may become much bigger over time.

The point is not that every company wins. The point is that your future is not tied to only one company’s success.

This is especially helpful for beginners who are still learning how to read businesses.

A broad ETF lets you start building wealth while you continue developing your investing skills.

Automation helps you invest even when the news is noisy

The hardest part of investing is often not choosing what to buy.

It is continuing when the world feels uncertain.

There will always be scary headlines: inflation, interest rates, elections, recessions, wars, layoffs, banking stress, technology disruption, and market crashes.

If your plan depends on feeling confident every month, you may never invest consistently.

That is why automation helps.

You can set a recurring transfer from your bank account to your brokerage account. In some cases, you can also set recurring investments into selected funds, depending on the platform and account type.

Major platforms such as Vanguard, Fidelity, and Charles Schwab offer beginner-friendly investing resources and account options, though availability depends on your country and personal situation.

The purpose of automation is not to remove thinking completely.

It is to remove repeated emotional decision-making.

Instead of asking every month, “Is now a good time?”

You follow the plan: “This is my long-term investing day.”

Dollar-cost averaging makes timing less stressful

Dollar-cost averaging means investing a fixed amount at regular intervals.

For example, you invest $200 every month into a broad ETF.

When the market is high, your $200 buys fewer shares.

When the market is low, your $200 buys more shares.

This approach is useful because beginners often get stuck waiting for the perfect moment. They want to invest, but they worry the market is too expensive. Then prices rise, and they regret waiting. Then prices fall, and they become afraid to start.

Dollar-cost averaging gives you a practical way out of that loop.

You stop trying to predict the perfect entry point and focus on building the habit.

This does not guarantee profits. Nothing does.

But it does help you avoid one of the most common beginner problems: investing only when you feel excited and stopping when prices are actually cheaper.

Your passive base gives you permission to learn slowly

A passive base is not just a financial tool. It is also a learning tool.

It gives you time.

Instead of rushing into individual stocks because you feel behind, you can let your core portfolio grow while you study businesses at a reasonable pace.

You can learn how to read annual reports. You can understand moats. You can study management. You can practice valuation.

And because your main wealth-building system is already running, you do not need to force every idea into action.

That is a calmer way to invest.

For beginners, this structure can be especially useful:

- Use passive ETFs as the foundation.

- Keep individual stock picking small or wait until you are ready.

- Never risk emergency money.

- Invest consistently.

- Learn before increasing complexity.

The goal is not to look clever this month.

The goal is to become the kind of investor who can stay in the game for decades.

Once that foundation is working, you can begin thinking more carefully about how to evaluate individual businesses without turning your portfolio into a guessing game.

Core and Satellite: A Portfolio Shape That Limits Regret

Once your passive investing base is running, the next question is not, “Which stock should I buy?”

A better question is, “How much of my portfolio should I allow myself to actively manage?”

That small change matters.

Many beginners jump from zero investing experience straight into picking individual stocks. They buy five companies, check prices every day, and feel like their entire financial future depends on whether those stocks go up this month.

That is too much pressure.

A core and satellite portfolio gives you a calmer structure.

Your core is the steady part of your portfolio. This is usually made up of broad, low-cost index funds or ETFs. It is designed to grow quietly in the background with very little effort.

Your satellites are the smaller, more active part. This is where you might buy individual businesses you have researched carefully.

Think of it like a meal.

The core is the main dish. It gives you the nutrition. It keeps you full. The satellites are the seasoning. They can make the meal better, but they should not be the entire meal.

Why the core comes first

The core protects you from one of the most common beginner problems: overconfidence.

When someone gets interested in investing, it is natural to want to find “the next big winner.” Maybe it is an AI stock, a clean energy company, a fintech platform, or a famous brand everyone talks about.

But finding great individual stocks is not easy.

Even professional investors struggle to beat the market consistently. So for beginners, it makes sense to build a broad foundation first.

A simple passive core helps you:

- Stay invested without needing to predict the market

- Spread risk across many companies

- Avoid depending on one stock to build wealth

- Keep investing even while you are still learning

- Reduce regret if one individual stock performs badly

The money outcome is practical: your wealth-building plan does not stop just because your stock-picking skills are still developing.

You can keep learning without putting your entire future on the line.

How much should go into satellites?

There is no perfect split for everyone.

A beginner who wants a simple life may choose a 100% passive portfolio. That is completely valid. You do not need to pick individual stocks to be a real investor.

Someone who enjoys studying businesses may prefer a blended approach.

For example:

- 100/0 portfolio: 100% passive core, 0% individual stocks

- 80/20 portfolio: 80% passive core, 20% active stock picking

- 70/30 portfolio: 70% passive core, 30% active stock picking

- 60/40 portfolio: 60% passive core, 40% active stock picking

The more active your portfolio becomes, the more responsibility you take on.

A 60/40 split is not just “more exciting.” It means you need to spend more time reading annual reports, understanding business models, checking valuation, and reviewing your decisions.

For most beginners, an 80/20 structure is a sensible starting point if they want to try individual stocks.

It gives you room to learn without letting one mistake damage the whole plan.

The regret test for choosing your split

Here is a simple way to choose your allocation.

Ask yourself two questions:

- If my individual stocks do badly for three years, will I still sleep well?

- If my passive core does better than my stock picks, will I still follow the plan?

If the answer is no, your satellite portion is probably too large.

A good portfolio is not just mathematically reasonable. It must also fit your temperament.

The best investing strategy is the one you can actually stick with when the market becomes uncomfortable.

Buffett’s Bargains: Four Filters Before You Buy Any Business

Once you have decided to make room for individual stocks, the next step is to slow down.

Not every famous company is a good investment.

Not every growing company is worth buying.

And not every falling stock is a bargain.

Buffett-style investing is not about buying random cheap stocks. It is about looking for wonderful businesses at sensible or discounted prices.

Before buying any individual stock, run it through four filters.

Filter 1: Can you understand the business?

This is the first gate.

Before buying a stock, you should be able to explain the company in plain English.

Not with buzzwords. Not with copied language from the company website. Plain English.

Try answering these questions:

- What does the company sell?

- Who are its customers?

- How does it make money?

- Why do customers choose it?

- What could hurt the business?

- What would make profits grow over time?

If you cannot answer these questions, skip it for now.

That does not mean the company is bad. It simply means it may be outside your current understanding.

For example, you may understand a retailer, restaurant chain, payment app, or streaming business more easily than a biotech company developing highly technical treatments.

That is okay.

Beginners do not need to understand every industry. They need to know the boundaries of what they understand.

A missed opportunity is less painful than owning a business you cannot judge.

Filter 2: Does the business have a moat?

A moat is a durable competitive advantage.

In simple terms, it means the business has something that makes it hard for competitors to attack.

Without a moat, a profitable company can quickly attract competition. Competitors lower prices, copy products, spend more on marketing, and fight for customers. Over time, profits can shrink.

A moat helps protect the castle.

Common moats include:

- Brand: Customers trust the name and pay more for it.

- Switching costs: Customers do not want the hassle of leaving.

- Network effects: The product becomes more useful as more people use it.

- Scale advantage: The company can operate cheaper because it is so large.

- Toll position: Other businesses must use its platform, marketplace, or infrastructure.

- Secret sauce: The company has unique technology, patents, data, or expertise.

A company like Apple is often discussed as a business with multiple advantages: brand loyalty, ecosystem stickiness, and deep product integration.

A company like Amazon has scale, logistics strength, marketplace effects, and customer habits built over many years.

The beginner lesson is not “buy Apple or Amazon.” The lesson is to look for businesses where the advantage is obvious enough that you can explain it.

If you have to invent a complicated story to justify the moat, be careful.

Filter 3: Can you trust management?

A business can look great on paper and still be a poor investment if the people running it make bad decisions.

Management matters because leaders decide what happens to the company’s profits.

They can reinvest in growth, pay down debt, buy back shares, pay dividends, make acquisitions, or waste money chasing ego projects.

For beginners, management can feel hard to judge, but you can start with simple clues.

Look for:

- Clear shareholder letters

- Honest discussion of mistakes

- Sensible debt levels

- Smart use of cash

- Consistent long-term strategy

- Leaders who own meaningful shares

- Compensation tied to long-term performance

Also watch for warning signs:

- Constant hype with little substance

- Frequent strategy changes

- Heavy debt with weak cash flow

- Large acquisitions that seem unrelated

- Management blaming everyone else when results disappoint

- Buybacks at obviously inflated prices

You are not just buying a stock ticker. You are partnering with the people who make decisions on your behalf.

Choose partners carefully.

Filter 4: Is the price attractive enough?

A great business can still be a bad investment if you overpay.

This is one of the hardest ideas for beginners because strong companies often feel “safe” at any price.

But price matters.

Imagine buying a small coffee shop. The shop is profitable, popular, and well-run. That sounds good.

But would you pay $10 million for it if it only earns $100,000 per year?

Probably not.

The same idea applies to stocks.

You want to estimate what the business is reasonably worth, then buy only when the market price gives you a margin of safety.

You do not need perfect math to understand the principle.

If a business is worth around $100 per share, buying at $95 gives you very little room for error. Buying at $70 gives you more room. Buying at $50 gives you even more.

That discount protects you from imperfect estimates, bad luck, and unexpected problems.

Moat, Management, and Margin of Safety Without Finance Jargon

Finance can sound intimidating because people often explain simple ideas with complicated words.

But the heart of Buffett-style investing is not that complicated.

You are trying to answer three plain questions:

- Is this business hard to compete with?

- Are the people running it smart and trustworthy?

- Can I buy it at a price that gives me room to be wrong?

That is moat, management, and margin of safety.

How to spot a moat in real life

Start with everyday behavior.

Ask yourself: “Why do customers keep choosing this company?”

For example:

- Do people buy it because they trust the brand?

- Would switching to a competitor be annoying or expensive?

- Does the service become better as more users join?

- Can the company offer lower prices because of its size?

- Does it own a platform other businesses need?

Then check whether the numbers support the story.

You do not need to become a Wall Street analyst overnight. Start with three beginner-friendly checks.

First, look at gross margin.

Gross margin shows how much money a company keeps after the direct cost of producing its product or service.

A lemonade stand example makes this simple.

If one cup sells for $5 and the ingredients cost $3, the gross profit is $2. That means the gross margin is 40%.

A high gross margin compared with direct competitors can suggest pricing power, brand strength, or a cost advantage.

But compare companies within the same industry. A software company and a supermarket naturally have different margins.

Second, look at revenue growth and operating margin.

Revenue is total sales. Operating margin shows how much profit the business keeps after normal operating costs.

A strong sign is when a company grows sales and improves profitability over time.

That means the company is not just getting bigger. It is becoming more efficient as it grows.

Third, look at return on invested capital, often called ROIC.

Do not let the term scare you.

ROIC asks: “When the company reinvests money into the business, does it generate strong returns?”

A business with high and stable ROIC may have a real advantage. It can put money to work and produce attractive profits.

For beginners, the goal is not to calculate everything perfectly on day one. The goal is to learn what the numbers are trying to reveal.

A moat should show up in customer behavior and business results.

How to judge management without pretending to know everything

You cannot know a CEO personally just by reading reports.

But you can study behavior.

The most important question is: “Do they treat capital like owners?”

Good managers understand that every dollar belongs to shareholders. They do not spend money just to look busy. They put money where it can create long-term value.

A practical beginner checklist:

- Read the latest shareholder letter.

Does management explain results clearly, or hide behind buzzwords? - Check debt.

Is the company taking on too much risk? - Look at reinvestment.

Are profits being used to grow the business at attractive returns? - Study buybacks.

Is the company buying back shares when they are reasonably priced, or wasting cash when the stock is expensive? - Review consistency.

Does management follow a clear long-term plan, or chase every trend?

You can find company filings through investor relations pages or SEC EDGAR.

Do not rush this step.

A strong moat with poor management can become a wasted opportunity. A decent business with excellent capital allocation can sometimes surprise you. But the ideal combination is a strong business run by capable, honest people.

Why margin of safety is your emotional cushion

Margin of safety is usually explained as a valuation concept.

But for beginners, it is also an emotional tool.

When you buy a business at a discount to your estimate of value, you are not depending on everything going perfectly.

That matters because the future is messy.

Sales may grow slower than expected. A competitor may get stronger. Interest rates may rise. A product launch may disappoint. Management may make a mistake.

A margin of safety gives your investment room to survive normal imperfection.

It also makes you calmer.

If you buy a stock at what you believe is a discount, a short-term price drop is easier to handle. You can go back to your analysis and ask whether the business changed.

Without a margin of safety, every drop feels personal.

You feel like the market is telling you that you were wrong.

With a margin of safety, you are more likely to think like a business owner instead of a nervous trader.

Buying and Selling Rules That Protect You From Your Own Mood

Most investors do not get into trouble because they lack information.

They get into trouble because they make decisions while emotional.

They buy when excited. They sell when scared. They hold losers because they do not want to admit mistakes. They sell winners too early because they want to “feel smart.”

Rules help you avoid that.

Rules are not there to make investing boring. They are there to keep your future self from undoing your present plan.

Rules for your passive core

Your passive core should be simple.

The goal is not to trade it. The goal is to keep building it.

Use these rules:

- Invest only what you can repeat.

Choose an amount that fits your real cash flow. - Buy on schedule.

Do not wait for perfect headlines. - Do not sell because the market is noisy.

Market drops are part of the journey. - Review the plan, not the price, too often.

Monthly or quarterly is usually enough for most beginners.

This is how the core does its job.

It compounds in the background while you focus on earning, saving, learning, and living.

Rules before buying individual stocks

Individual stocks need stricter rules because the risk is more concentrated.

Before buying, write a short investment note.

It does not need to be fancy. One page is enough.

Include:

- What the company does

- Why you understand it

- What moat you believe it has

- Why management seems trustworthy

- What you think the business is worth

- Your margin of safety price

- What would make you sell

This small habit can prevent many bad decisions.

It forces you to slow down.

It also gives you something to review later. If the stock falls, you can compare the new facts with your original reason instead of reacting to fear.

When to sell without panic

Selling should not be based on mood.

It should be based on facts.

A few sensible reasons to sell include:

- The business is no longer as strong as you thought.

- The moat is weakening.

- Management has become reckless or dishonest.

- Debt has become dangerous.

- The company has changed into something you no longer understand.

- The stock price has risen far beyond a reasonable estimate of value.

- You found a much better opportunity and need to reallocate capital.

Notice what is not on the list:

“The stock fell this week.”

A falling price alone is not a sell reason.

Sometimes a falling price is a warning. Sometimes it is an opportunity. The difference depends on whether the business has changed.

That is why your written investment note matters.

When holding is the smarter move

There is also a danger in selling too quickly.

Some of the best long-term investments are businesses that keep getting better for years. If you sell every winner the moment it becomes slightly expensive, you may cut off the very companies that could do the most work in your portfolio.

This is where judgment comes in.

If a stock has become wildly overvalued, selling can be rational.

But if the business remains exceptional, the moat is intact, management is still strong, and the company has a long growth runway, holding may also be rational.

The key is not to hold because you are emotionally attached.

Hold because the business still deserves your capital.

The mood-proof decision checklist

Before any buy or sell decision, ask:

- Am I acting from analysis or emotion?

- Has the business changed, or only the price?

- Does this decision match my written rules?

- Would I make the same decision if the market were closed for one year?

- Am I protecting my long-term plan or chasing short-term comfort?

These questions slow you down.

And slowing down is often where better investing decisions begin.

Your passive core gives you stability. Your satellite investments give you room to pursue higher-upside opportunities. But your rules are what keep both parts working together when the market gets loud.

In the next section, the plan becomes even more personal: choosing the path that fits your time, confidence, income, and current stage of life.

Choose the Path That Matches Your Time, Money, and Confidence

The best investing plan is not the one that looks impressive on paper.

It is the one you can actually follow when life gets busy, the market gets noisy, and your motivation drops.

A beginner with $100 a month should not copy someone investing $10,000 a month. A freelancer with unpredictable income should not copy someone with a stable salary and low expenses. A busy parent should not copy an investor who reads annual reports for fun every weekend.

Rational investing starts with honesty.

You need a path that fits your real life, not your fantasy version of yourself.

If you are starting with very little money

If you are new to investing and only have a small amount to invest, do not feel behind.

Small amounts are enough to build the habit.

Your first goal is not to “get rich” from one investment. Your first goal is to become the kind of person who saves, invests, and avoids emotional decisions.

Start with three simple actions:

- Clear any high-interest debt first.

- Build at least a starter emergency fund.

- Set a small monthly investing amount you can repeat.

That amount could be $25, $50, or $100.

The number matters less than the repeatability.

Your first measurable win is not a huge portfolio. It is completing three months of consistent investing without stopping, borrowing, or panic-selling.

That is how confidence starts.

If you have stable income but limited time

If you work full-time and do not want investing to become a second job, keep the plan simple.

A passive ETF-based approach may fit you well.

You can automate a monthly contribution, review your budget once a month, and spend a small amount of time learning the basics.

Your investing system might look like this:

- Monthly transfer into your brokerage account

- Broad ETF as your portfolio core

- Emergency fund kept separate

- One monthly review date

- No daily price checking

This path is not flashy, but it is powerful because it protects your attention.

Your time is valuable. If you can build wealth without turning every evening into stock research, that is a win.

The first measurable win here is having your investing habit run quietly in the background while your career and income keep growing.

If you want to research individual stocks

Some people enjoy studying businesses.

If that is you, individual stocks can become your satellite portfolio. But they should come after your foundation, not before it.

Your job is to earn the right to buy individual businesses by doing the work first.

Before buying, write down:

- What the company does

- Why customers choose it

- What advantage protects the business

- Why management seems trustworthy

- What price gives you a margin of safety

- What would make you sell

This does not need to be a 30-page report. A clear one-page note is already better than most beginner decisions.

Your first measurable win is not picking a winning stock immediately.

It is rejecting a stock because your research was not strong enough.

That may sound strange, but it is a real sign of progress. It means you are no longer buying every exciting idea that crosses your screen.

If your income is irregular

Freelancers, creators, contractors, and commission-based workers need a slightly different setup.

Your biggest risk is not only market volatility. It is cash flow volatility.

Some months are great. Other months are slow.

That means your emergency fund should usually be larger. You may also prefer investing a percentage of income instead of a fixed dollar amount.

For example:

- 10% of every paid invoice goes to taxes

- 10% goes to emergency savings until fully funded

- 5% goes to investing

- The rest covers living and business expenses

Adjust the percentages to fit your situation.

The key is to create rules before money arrives. Otherwise, a strong month can disappear into random spending.

Your first measurable win is turning irregular income into a repeatable money system.

A 7-Day Sprint to Turn This Into a Real Investing System

You do not need to fix your entire financial life in one weekend.

But you can build the skeleton of your investing system in seven days.

This sprint is designed for beginners. Keep it simple. Do not try to make perfect decisions. Try to make useful decisions you can improve later.

Day 1: Write down your real financial picture

Start with the truth.

Open your bank accounts, credit cards, loans, and savings accounts. Write down the numbers.

You need four things:

- Total cash

- Total debt

- Monthly income

- Monthly expenses

Do not judge yourself while doing this.

The goal is clarity, not shame.

Once everything is visible, mark any high-interest debt. That becomes your first financial enemy because it quietly works against your investing progress.

By the end of Day 1, you should know whether you are ready to invest now or whether your first step is debt reduction and cash stability.

Day 2: Build your safety net target

Now calculate your essential monthly expenses.

Include housing, food, utilities, transport, insurance, minimum debt payments, and basic family responsibilities.

Then choose your emergency fund target.

A simple guide:

- Stable income and low obligations: aim for three months

- Irregular income or family responsibilities: aim for six months

- Very unstable income: consider even more

You do not need to fully fund it today.

Just define the target.

Then create a starter goal. For example, your first emergency fund milestone might be $500, $1,000, or one month of essential expenses.

This gives you something achievable to work toward.

Day 3: Choose your monthly investing amount

Now pick an amount you can invest consistently.

Be realistic.

Do not choose a number that forces you to live on stress and willpower. That usually fails.

A good investing amount should feel slightly challenging but sustainable.

For example:

- If $300 feels stressful, start with $100.

- If $100 feels stressful, start with $25.

- If any amount feels impossible, focus first on income, expenses, and debt.

This is not a competition.

The goal is to create a habit that can survive real life.

Once the habit is stable, you can increase the amount later.

Day 4: Decide your portfolio structure

Choose your core and satellite split.

If you are a complete beginner, a 100% passive core is perfectly fine.

If you want to learn stock picking slowly, you might choose something like 90/10 or 80/20.

For example:

- 90% broad ETFs

- 10% individual stock research ideas

This structure protects you from overconfidence.

It lets your main plan stay steady while your learning happens in a controlled space.

Write your split down. Do not keep it vague.

Vague plans are easy to break.

Day 5: Create your buying rules

Before you buy anything, write your rules.

For your passive core, your rules might be:

- I invest monthly.

- I do not sell because of headlines.

- I only use money meant for the long term.

- I review the plan monthly, not daily.

For individual stocks, your rules might be:

- I only buy businesses I can explain simply.

- I must identify a moat.

- I must check management quality.

- I must estimate value before buying.

- I must have a margin of safety.

- I must write down the reason before buying.

These rules will feel unnecessary when everything is calm.

They become priceless when the market gets emotional.

Day 6: Remove obvious temptation

Your environment affects your behavior.

If you keep checking prices every hour, investing will feel like a game. If your social feed is full of hype, you will feel pressure to chase.

So remove friction from bad behavior.

You can:

- Turn off trading app notifications

- Stop following hype-driven accounts

- Avoid checking your portfolio daily

- Delete watchlists full of random “maybe” stocks

- Keep your written plan somewhere visible

This is not about being weak. It is about being smart.

Good systems make good behavior easier.

Day 7: Make one boring move

The final day is about action.

Make one simple move that supports your plan.

That could be:

- Setting up an automatic transfer

- Paying extra toward high-interest debt

- Moving money into your emergency fund

- Buying your first planned ETF investment

- Writing your first one-page stock research note

Choose one.

Do not try to do everything.

The goal is to leave the seven-day sprint with a real system, not just more information.

By the end, you should know where your money stands, what your first priority is, how much you can invest, and what rules will guide you.

That is already more structure than many beginners have.

Guardrails That Keep Beginners Out of the Casino

The stock market can be a powerful wealth-building tool.

But the same market can also become a casino if you approach it with the wrong behavior.

The danger is not the market itself. The danger is using serious financial tools with a gambling mindset.

Guardrails keep you from turning investing into entertainment.

Do not use money you need soon

This is the first guardrail.

If you need the money in the next few months or years, be careful about putting it into stocks.

The market does not move on your schedule.

Your home deposit, rent money, tax money, tuition money, or emergency fund should not depend on whether the market is having a good month.

A simple rule:

If selling during a downturn would create a life problem, that money should not be invested aggressively.

Long-term money can handle volatility better because it has time to recover. Short-term money needs stability.

Stay away from margin as a beginner

Margin means borrowing money to invest.

It can make gains look bigger, but it can also make losses more dangerous.

The biggest issue is forced selling.

If your investments fall too much, you may be required to add more money or sell positions at a bad time. That removes your control.

For beginners, this is unnecessary risk.

You are already learning how to manage emotions, understand businesses, and build consistency. Borrowed money adds pressure before you have enough experience.

A clean beginner rule:

No margin.

Build wealth with money you actually have.

Be very careful with options

Options are often marketed as a fast way to make money.

But they are complex. They can move quickly. They can expire worthless. They can create risks beginners do not fully understand.

That does not mean options are always bad. It means they are not a beginner foundation.

If you cannot clearly explain how an options trade makes money, how it loses money, what time decay means, and what your maximum risk is, do not use it.

There is no shame in skipping complicated tools.

Simple investing done consistently can beat complicated trading done emotionally.

A social media post can introduce you to a company.

That is fine.

But it should never be the reason you buy.

Someone online may have a different risk tolerance, portfolio size, time horizon, or hidden incentive. They may sell before you even realize the story changed.

Use online ideas like a starting point, not a command.

Before buying anything, ask:

- Do I understand the business?

- Have I checked the risks?

- Can I explain the moat?

- Do I trust management?

- Is the price reasonable?

- Does this fit my portfolio plan?

If the answer is no, do not buy yet.

Missing a stock is not a disaster. Buying blindly can be.

Do not confuse activity with progress

Many beginners think more action means better investing.

More trades. More alerts. More charts. More predictions.

But investing rewards good decisions, not constant motion.

Sometimes the best move is to do nothing.

If your emergency fund is healthy, your passive investments are automated, your debts are under control, and your rules are written, you may not need to touch anything today.

That can feel boring.

But boring is not bad.

Boring often means your system is working.

The Quiet Rules That Keep Your Money Working

The investors who build wealth over decades are not usually the loudest people in the room.

They are the ones who keep doing the right simple things when nobody is watching.

They save consistently. They avoid expensive mistakes. They buy with patience. They ignore most noise. They let time do its work.

This is where rational long-term investing becomes less about tactics and more about behavior.

Keep your plan small enough to follow

A complicated plan is easy to abandon.

If your investing system requires ten spreadsheets, daily research, constant valuation updates, and emotional perfection, it may not survive your actual life.

A strong beginner plan should fit on one page.

It should answer:

- How much do I invest each month?

- What do I buy for my core?

- How much can go into individual stocks?

- What must be true before I buy?

- When do I review?

- What would make me sell?

That is enough to begin.

You can improve the plan as your skills grow.

Review your portfolio on a schedule

Do not let your portfolio become something you check every time you feel anxious.

Create a review rhythm.

For many beginners, monthly is enough for budget and contribution checks. Quarterly or twice a year may be enough for deeper portfolio review.

During review, ask:

- Is my emergency fund still healthy?

- Is my debt under control?

- Am I investing consistently?

- Does my portfolio still match my target split?

- Have any individual stock facts changed?

- Am I acting according to my rules?

This keeps your attention on the plan instead of the noise.

Increase contributions before increasing complexity

When people want better results, they often look for more complicated strategies.

But for beginners, the biggest improvement may be much simpler: invest more consistently or increase the contribution amount when income rises.

If you get a raise, bonus, new client, or side income, decide in advance how much will go toward investing.

For example:

- 50% of every raise goes to investing

- 20% of every bonus goes to long-term wealth

- 10% of side income goes to the portfolio

This turns income growth into asset growth.

It also prevents lifestyle inflation from swallowing every improvement in your financial life.

Let time do the heavy lifting

Compounding needs time.

That is the part beginners often underestimate.

A few months of investing may not look exciting. A few years may still feel slow. But over long periods, consistent investing can create meaningful momentum.

The problem is that many people quit before the results become visible.

They get bored. They chase something faster. They panic during a downturn. They change strategies every few months.

Your advantage as a beginner is not predicting the future.

Your advantage is staying with a sensible plan long enough for it to matter.

What to Remember Before You Put Money to Work

- Choose an investing path that matches your real income, time, confidence, and emotional tolerance.

- Build a system before chasing individual stock ideas.

- Use a seven-day sprint to define your numbers, rules, portfolio structure, and first action.

- Keep emergency money and short-term goal money away from market risk.

- Avoid margin, complex options, and social media-driven buying as a beginner.

- Review your plan on a schedule, increase contributions when possible, and let time work quietly in the background.

The market will always be noisy. Your job is not to respond to every sound. Your job is to build a plan strong enough that you do not have to.

Disclaimer

This article is for educational and informational purposes only. It is not personal financial advice, investment advice, or a recommendation to buy or sell any stock, ETF, fund, or financial product.

Investing involves risk, including the possible loss of money. Everyone’s financial situation, goals, income, debt level, risk tolerance, and time horizon are different. Before making investment decisions, do your own research and consider speaking with a qualified financial advisor or licensed professional.

Any examples mentioned in this article are used only to explain investing concepts in a beginner-friendly way. They should not be treated as guaranteed results or specific investment recommendations.

Enjoyed this guide? ☕

If this article helped you feel a little clearer, calmer, or more confident about investing, you can support the blog by buying me a coffee. Your support helps me keep creating beginner-friendly guides that turn confusing money topics into practical steps you can actually use.

👉 Buy me a coffee ☕✨

{kind=link}