Financial Risk Myths: The Dangerous Lies Keeping You Broke 🚨

Financial risk myths are quietly shaping the way you save, spend, and invest—often without you noticing. One “safe” choice here, one “high-return opportunity” there, and suddenly your money is exposed to risks you never planned for… or it’s sitting still while everything around you gets more expensive.

If you’ve ever felt torn between “don’t risk anything” and “take bold risks to get rich,” this guide is for you. We’re going to strip away the hype, decode the jargon, and show you how to think about risk in a way that actually helps you protect and grow your money.

By the end, you’ll be able to spot bad advice and scams faster, understand what kind of risk you’re really taking, and build a simple plan that fits your real life—not some fantasy screenshot on social media.

Why There Is So Much Hype and Confusion Around This Topic

If you’ve spent any time on YouTube, TikTok, or finance Twitter, you’ve probably noticed something strange: everyone has a completely different “truth” about risk and how to “play” the money game.

One voice shouts, “Just save cash, investing is gambling.”

Another says, “Go all in on this stock or coin, it’s a once-in-a-lifetime opportunity.”

Someone else claims, “My AI bot makes profits with no risk at all.”

If you feel torn between these messages, that’s not a personal failure. The problem is that risk is invisible, emotional, and very easy to use as a sales tool.

Here are the main reasons there’s so much hype and noise around financial risk:

- Risk is hard to see until it explodes.

When prices are going up, almost every strategy looks smart. You don’t see who’s secretly taking crazy risk in the background. You only hear about them when everything crashes. - “No risk” headlines sell better than “managed risk.”

“Make 8–10% a year with a boring diversified portfolio” doesn’t go viral.

“Turn $500 into $5,000 in 30 days” spreads like wildfire.

So creators, salespeople, and even some platforms exaggerate how safe and profitable something is. - The language of risk is often deliberately complex.

You’ll see words like volatility, derivatives, hedging, exposure, correlation. If you’re new, it sounds like a foreign language. Jargon makes normal people feel dumb, so they stop asking questions and just “trust the expert.”

Put all of this together and beginners fall into a few expensive habits:

- Trusting whoever sounds the most confident

- Confusing complex with safe

- Making money decisions based on vibes instead of clear understanding

This confusion has real costs. It can make people:

- Keep most of their money in cash “for safety,” and slowly lose to inflation

- Throw their savings into one hot trend because “everyone” is doing it

- Buy financial products they don’t understand, just because a “guru” or friend recommended them

The result? Many people either get stuck and never invest at all, or they take wild risks without realizing it. Both paths can quietly keep you broke or stressed for years.

The good news is you don’t need advanced math or a finance degree to step out of this trap. You just need a clearer, more honest view of what risk is and how it shows up in your life.

Once you see risk more clearly, you can start making money decisions that are simple, sensible, and actually aligned with your goals instead of someone else’s marketing.

A Quick Reality Check: What Financial Risk Really Is (and Is Not)

Before we dive into myths and red flags, we need a solid foundation. Let’s give “financial risk” a simple, practical definition you can actually use in everyday decisions.

What Financial Risk Actually Is

In plain language, financial risk is the chance that reality turns out worse than you expected, in money terms.

That could mean:

- Your investment drops in value

- Your income is lower than you planned

- Your costs suddenly spike (illness, accident, job loss, divorce)

- A business or project earns less than you hoped

Risk is not just the chance of a total disaster. It’s any meaningful gap between what you expected and what actually happens.

There are many types of financial risk, but as a beginner you can think in simple categories:

- Market risk – prices in the stock, bond, or crypto market move against you

- Income risk – you lose a client, job, or source of cash flow

- Liquidity risk – your money is locked up and you can’t access it when you need it

- Credit risk – someone who owes you money doesn’t pay you back

You don’t need to memorize these labels. What matters is this question:

“What could realistically go wrong here, and how would that affect my money?”

That one question is already a big step toward thinking like a responsible investor instead of a gambler.

What People Wrongly Believe Financial Risk Is

A lot of money mistakes come from false ideas about risk. Here are some of the most common ones:

- “Risk = gambling.”

Many people think investing is basically a casino. That’s not true. Gambling is designed so the house always wins. Investing is owning real businesses, assets, or cash flows. It can still be risky, but it’s not the same as pulling a lever on a slot machine. - “Risk only matters if I’m doing something extreme.”

People think risk management is just for traders using leverage or day trading crypto. In reality, you face risk even if you only have a job, a savings account, and basic bills. Job loss, health issues, or inflation can hurt you even if you never touch the stock market. - “Safe means zero risk.”

Beginners often think cash is “risk-free” and everything else is “risky.” But holding too much cash for too long exposes you to inflation risk. Over years, that can quietly steal a big chunk of your purchasing power. - “If it’s complex, it must be safer or smarter.”

A product with a long brochure and fancy formulas can feel “professional.” But complexity can hide risk instead of removing it. If you don’t understand how something works, you can’t judge the risk properly.

These beliefs make people either freeze (“I’ll never invest, it’s too risky”) or do reckless things (“This complex product must be safer, I’ll put everything into it”).

Where Understanding Risk Genuinely Helps You Make Better Money Choices

So why should you care about this more than just theory? Because a basic grasp of risk changes how you move with money.

Here’s how understanding risk helps you in real life:

- You stop falling for impossible promises.

When you accept that higher potential returns always come with some type of risk, it becomes much easier to reject “guaranteed 3% daily” or “no-loss” schemes. - You make smarter trade-offs.

You’ll see that every choice has a cost. Keeping too much cash feels safe but has inflation risk. Going heavy into one stock has concentration risk. Once you see those trade-offs, you can design a mix that fits your personality and goals. - You protect your future self.

Instead of only asking “How much can I gain?”, you also ask, “What happens if this goes badly?” That small shift leads you to build an emergency fund, get basic insurance, and avoid bets that could wipe you out. - You stay in the game longer.

The people who end up wealthy are often not the ones with the flashiest wins. They’re the ones who avoid massive, crippling losses. Understanding risk helps you avoid the kind of mistake that wipes out years of progress.

You don’t have to become a risk analyst. You just have to be curious and honest about what could go wrong, and intentional about what you’re willing to risk.

From here, it becomes much easier to look at specific myths and red flags with clear eyes—and to start using simple risk thinking as a tool to protect and grow your money instead of letting hype push you around.

Big Myths That Keep You Stuck or Broke

When you don’t really understand financial risk, it’s easy to build your entire money life on half-truths and catchy slogans. These financial risk myths sound smart on social media, but in real life they quietly drain your savings, increase your stress, and block you from building real wealth.

In this section, we’ll unpack some of the biggest financial risk myths beginners fall for. As you read, don’t just think “other people do this.” Ask yourself honestly: Where am I acting based on this myth? That’s where you have the fastest opportunity to improve your money decisions.

Myth 1: “Playing It Safe Means Avoiding All Risk”

The myth in one sentence:

If you’re smart and responsible, you avoid risk completely—especially with money.

Why people believe it:

Most of us grew up hearing “Don’t risk it,” “Better safe than sorry,” or “Investing is gambling.” If we’ve seen family or friends lose money, the lesson feels obvious: risk = pain. So the “safe” option becomes: keep everything in cash and never invest.

The truth:

Avoiding all risk is itself a big risk.

If you keep all your money in a basic savings account “for safety,” inflation slowly eats away its value. Your bank balance stays the same, but what that money can buy shrinks over time. If you also avoid investing in your skills or assets, your income may stay flat while prices rise.

Responsible financial risk management doesn’t mean avoiding risk. It means choosing which risks you take, and how much, for what potential benefit.

How this myth hurts your money:

- You miss out on years of compound growth by never investing.

- You stay dependent on one income source, which is risky by itself.

- You become more vulnerable to inflation and unexpected expenses.

Do this instead:

- Accept that there is no zero-risk option—only different types of risk.

- Protect essentials (rent, food, emergency fund), then invest a portion of what’s left for the long term.

- Start small with simple, diversified investments instead of waiting for a “risk-free” moment that never comes.

Myth 2: “More Risk Automatically Means More Reward”

The myth in one sentence:

If high risk equals high return, then taking maximum risk is the smartest way to get rich faster.

Why people believe it:

You see quotes like “Fortune favors the bold” and stories of people who went all in on one stock or coin and made a fortune. It’s easy to connect the dots: big risk = big win. So if you want big results, you just crank up the risk, right?

The truth:

Higher risk doesn’t promise higher returns; it just widens the range of outcomes.

You increase the chance of a big win and the chance of a big loss. The market doesn’t owe you a reward just because you took a big risk. Reckless risk-taking usually leads to losing money faster, not getting rich faster.

Professionals don’t just ask “How high could this go?” They also ask, “What’s the realistic worst case?” and “Can I survive that outcome?”

How this myth hurts your money:

- You put way too much into one hot asset, like a single stock or coin.

- You’re tempted to use leverage (borrowed money) without a safety plan.

- A few bad moves can wipe out months or years of savings.

Do this instead:

- Treat risk as something to measure and size, not something to max out.

- Limit how much of your net worth goes into any single investment or aggressive strategy.

- Focus on steady, repeatable returns rather than chasing rare jackpots.

Myth 3: “If I Diversify, Nothing Bad Can Happen”

The myth in one sentence:

As long as I spread my money around, I’m safe from serious losses.

Why people believe it:

Everyone repeats “Don’t put all your eggs in one basket,” so beginners assume that having lots of different investments equals safety. If they hold many coins, many stocks, or multiple side hustles, it feels like they’re protected.

The truth:

Diversification helps, but it’s not a magic shield. What really matters is what you’re diversified into.

If everything you own is tied to the same story—like a group of tech stocks that all crash when tech sentiment changes, or a pile of memecoins that all tank when crypto hype dies—that’s not real diversification. You just own many versions of the same risk.

True diversification means spreading your money across assets that don’t all move the same way for the same reasons.

How this myth hurts your money:

- You feel falsely safe because you own “lots of things,” but they’re highly correlated.

- When that one theme falls, your entire portfolio gets hit at once.

- You may hold too many positions to even track what you own and why.

Do this instead:

- Look beyond the number of positions and ask, “What makes these rise or fall?”

- Mix different types of assets (for example: broad stock funds, some bonds, a bit of cash, maybe real estate or a small business).

- Keep your portfolio simple enough that you can explain your diversification in a few clear sentences.

Myth 4: “Complex Products Are Safer Because Experts Designed Them”

The myth in one sentence:

If a financial product has complicated math and a 30-page brochure, it must be safer and smarter than simple options.

Why people believe it:

We tend to equate complexity with expertise. If a bank or platform offers something with graphs, formulas, and technical language, it feels “professional.” It’s easy to think: “Smart people built this, so they must have handled the risk.”

The truth:

Complex products often hide risk instead of eliminating it.

Sometimes, complexity is used to bundle different types of risk in ways that are hard to see. Even professionals have misjudged highly complex products and suffered huge losses when markets behaved differently than their models predicted.

If you don’t understand how something makes money, when it loses money, and who takes the other side, you’re flying blind.

How this myth hurts your money:

- You sign up for structured products, “capital protected” notes, or yield schemes without understanding the downside.

- You underestimate what can happen in extreme situations because the documentation focuses on “typical” scenarios.

- You give up control and rely entirely on marketing claims and glossy PDFs.

Do this instead:

- Make it a rule: if you can’t explain the product in simple language to a friend, you don’t put serious money into it.

- Ask specific questions: “In the worst realistic case, what happens to my money?” and “What are the fees and hidden conditions?”

- Remember that plain, transparent instruments (like low-cost index funds or simple insurance) often serve you better than flashy, engineered products.

Myth 5: “A Great Past Performance Chart Means a Safe Future”

The myth in one sentence:

If something has performed well for several months or years, it’s probably safe to join now.

Why people believe it:

Humans love patterns. When we see a chart that goes up and to the right, our brain says, “This thing wins. It will likely keep winning.” Many sales pages show impressive backtests or historical returns to tap into this feeling.

The truth:

Past performance is useful information, but it is not a guarantee of future results. Markets evolve, rules change, and strategies that worked in one environment can fail in another.

“Backtested” results are especially risky to trust blindly. They’re often built by tweaking a strategy after seeing the past data, which can make it look much more reliable than it really is.

How this myth hurts your money:

- You buy in at the top of a trend because you’re convinced the good times will continue.

- You ignore risk controls because “this method has never had a big loss before.”

- You’re shocked and unprepared when the strategy or asset finally has a rough period.

Do this instead:

- Treat past performance as a clue, not a promise.

- Ask how the strategy might behave in very different conditions (for example, a recession or a change in regulations).

- Assume there will be losing periods, and plan ahead for how you’ll respond when they arrive.

Myth 6: “Leverage Is Just a Shortcut for Small Investors”

The myth in one sentence:

Using margin, options, or other forms of leverage is simply a way for small investors to catch up and boost returns.

Why people believe it:

Many platforms make leverage look simple and exciting. “Control $10,000 of assets with just $1,000!” For someone starting with a small account, that sounds like a clever hack to speed up wealth-building.

The truth:

Leverage magnifies everything—including your mistakes.

If the underlying asset moves against you, losses are multiplied. A modest drop can trigger margin calls or forced liquidations that close your position at a terrible time. You don’t just lose your initial investment; you may owe more money on top of it.

Leverage isn’t evil, but it’s a power tool. Professionals use it with strict risk limits and hedging. Beginners usually use it emotionally, with little planning.

How this myth hurts your money:

- You open oversized leveraged positions that your account cannot support.

- Normal market swings cause panic or forced exits.

- A few bad trades erase your capital, and sometimes even leave you with debt.

Do this instead:

- If you’re a beginner, consider a simple rule: no leverage until you have a solid track record with unleveraged investing.

- If you later choose to use leverage, keep it very modest and only with money you can afford to lose.

- Focus on increasing your income and savings rate instead of trying to “hack” your way to wealth with dangerous shortcuts.

Myth 7: “If an Expert Recommends It, the Risk Must Be Under Control”

The myth in one sentence:

If a financial advisor, influencer, or “AI-powered platform” recommends something, they must have fully checked the risk for you.

Why people believe it:

We’re busy. It feels efficient to outsource decisions to people who seem confident and knowledgeable. Plus, if everyone in a certain community is doing the same thing, it feels safer to just follow.

The truth:

No one cares about your money as much as you do.

Advisors can be biased by commissions or company products. Influencers can be paid for promotions or simply lack deep understanding. Even well-meaning experts can be wrong, especially when conditions change.

Listening to others for ideas is fine. Handing them full responsibility without understanding the downside is not.

How this myth hurts your money:

- You buy products or join schemes that mainly benefit the seller, not you.

- You feel betrayed when something goes wrong, but you’re still the one who takes the loss.

- You never build your own risk judgment, so you remain dependent on others.

Do this instead:

- Treat every recommendation as a starting point for your own research, not as the final verdict.

- Ask advisors and platforms to explain risks and worst-case scenarios in plain language. If they can’t or won’t, that’s a red flag.

- Build the habit of saying, “I’ll think about it,” then reviewing the offer calmly on your own.

When you start spotting these financial risk myths in your own thinking, a lot of confusing money advice suddenly makes more sense. In the next part of this guide, we’ll zoom in on specific red flags that often show up in real-world offers, platforms, and “opportunities,” so you can protect your wallet before you put any money on the line.

Red Flags: Signs You’re About to Get Scammed or Misled

By now you’ve seen that risk itself isn’t evil. The real danger is taking bad risk without realising it—especially when someone else is nudging you into it for their own benefit.

Scams and misleading offers almost always follow certain patterns. Once you know these patterns, you’ll feel a lot calmer looking at any “opportunity,” whether it’s AI trading, crypto, online courses, or some fancy financial product.

Think of this section as your early-warning radar.

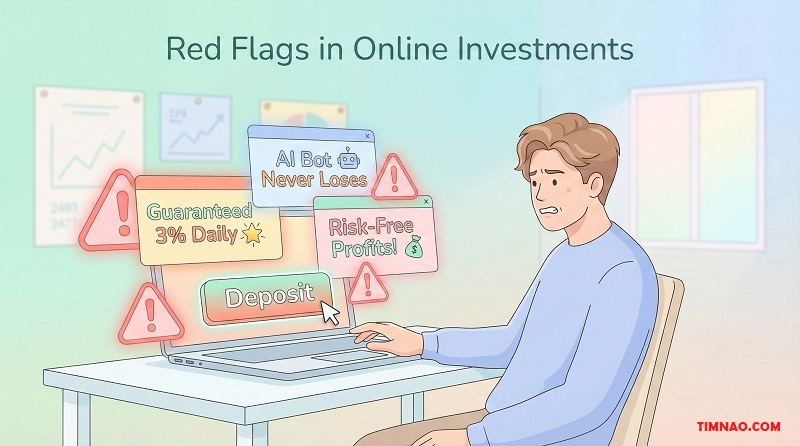

Red Flag 1: “Guaranteed” or “Risk-Free” High Returns

If you see phrases like:

- “3% daily, guaranteed”

- “Zero risk, only upside”

- “Our system has never lost”

…you should treat that as a massive warning sign, not a selling point.

No legitimate investment can offer high returns with zero risk. There is always some kind of trade-off: volatility, liquidity, credit risk, business risk, something. When someone deletes the downside from the story, they are either naive or dishonest.

How this threatens your money:

- You’re tempted to put in more than you can afford to lose because “it’s safe.”

- Early “profits” (often just numbers on a screen) make you overconfident.

- When the scheme collapses, you lose a big chunk of your savings, not just “play money.”

How to stay safe:

- Treat “guaranteed” + “high return” as an automatic deal-breaker.

- Ask, “What happens in a bad month or a bad year?” If they don’t have a clear, realistic answer, walk away.

- Remember: if the story sounds like a cheat code that bypasses risk, it’s not for you.

Red Flag 2: No Clear Explanation of How Money Is Made

A lot of shady projects use vague language:

- “Our AI trades using a secret algorithm.”

- “We leverage proprietary strategies.”

- “Profits are generated by a unique ecosystem.”

But when you ask, “Okay, but how exactly is the profit created?” the answer is either confusing or evasive.

If you can’t figure out who pays, for what, and why, you’re being asked to invest in pure mystery.

How this threatens your money:

- You’re funding a black box. If it stops paying, you have no idea why.

- You can’t judge whether the returns are realistic or sustainable.

- You’re more likely to stay in too long because you don’t see warning signs early.

How to stay safe:

- Ask yourself: “If I had to explain this to a teenager in one paragraph, could I?”

- Look for real economic activity: products sold, services delivered, actual customers.

- If the answer boils down to “just trust the system,” you don’t need it in your life.

Red Flag 3: Pressure, Urgency, and FOMO Tactics

Scammers and aggressive marketers hate it when you think clearly. So they create pressure:

- “Only 10 spots left.”

- “Price doubles at midnight.”

- “If you wait, you’ll miss the next big pump.”

Urgency shuts down your rational brain and activates fear of missing out. You’re pushed to decide now, not after you’ve had time to check details.

How this threatens your money:

- You skip basic checks (Who runs this? Is it regulated? How is money made?).

- You commit more money than you’re comfortable with because you feel rushed.

- You end up regretting the decision but feel ashamed to admit it.

How to stay safe:

- Adopt a personal rule: “I don’t invest under time pressure.”

- If a deal is good today, it should still be good after 24–48 hours of thinking.

- Treat extreme urgency as a test: if they won’t let you think, you don’t need them.

Red Flag 4: You Earn More by Recruiting Than by the Actual Product

Some systems pay you mainly for bringing in new people, not for any real value being created. The “product” is often overpriced, low-quality, or just a cover.

Signs to watch:

- Most of the pitch is about “building your team” and “downlines.”

- Earnings examples focus on how many people you’ve recruited, not what customers actually buy.

- Without new recruits, the whole thing barely makes money.

How this threatens your money:

- You’re essentially in a pyramid-style structure that depends on constant new sign-ups.

- When recruitment slows, income drops sharply and late joiners get burned.

- You risk damaging relationships by dragging friends and family into a shaky system.

How to stay safe:

- Ask, “If I never recruit anyone, can I still earn a reasonable amount from real customers?”

- Look at the product on its own: would you buy it at full price even if there were no “opportunity”?

- Be extra cautious of any plan where most success stories come from top recruiters.

Red Flag 5: No Transparency, No Control, Hard to Withdraw

Another big warning sign is when you’re asked to give up control without clear visibility:

- You send money to a wallet or platform, but there’s no proper account dashboard.

- You can’t see detailed transaction history.

- Withdrawals are slow, blocked, or constantly “under maintenance.”

Sometimes platforms stall withdrawals with excuses: system upgrades, audits, regulators, hackers—anything to keep your money in.

How this threatens your money:

- You may be funding a pool that’s used for risky bets or flat-out theft.

- By the time you realise something is wrong, you can’t get your money back.

- You feel trapped and might even put in more because “it will be fine after the issue is fixed.”

How to stay safe:

- Prefer platforms where you can clearly see balances, transactions, and terms.

- Start with small amounts and test withdrawals before you increase deposits.

- Treat consistent withdrawal issues as your cue to reduce exposure, not to wait patiently forever.

Red Flag 6: They Attack Anyone Who Asks Basic Questions

Pay attention to how people react when you ask fair questions like:

- “What are the main risks?”

- “How do you get paid from this?”

- “Is this regulated anywhere?”

If the response is:

- “You’re just negative / a hater / not ready to succeed.”

- “You ask too many questions—this isn’t for you.”

- “People who doubt never get rich.”

…then they’re trying to control you emotionally instead of giving honest answers.

How this threatens your money:

- You feel ashamed or “less than” if you hesitate, so you silence your doubts.

- You join a cult-like environment where critical thinking is punished.

- You stay in losing situations longer because you don’t want to be “the negative one.”

How to stay safe:

- Trust your questions. If something feels off, it probably is.

- Expect any serious financial offer to handle tough questions calmly.

- Walk away from any person or group that tries to bully you into compliance.

When you combine these red flags, you start to see patterns. Most bad deals aren’t original—they just repackage the same tricks with new buzzwords like “AI,” “Web3,” or “passive income.” Once you know what to look for, it becomes much easier to say “no” quickly and confidently.

What Actually Works: Principles That Stand the Test of Time

After reading about scams and red flags, it’s easy to feel like everything is dangerous. But that’s not true either. The point isn’t to fear all risk; it’s to lean into the right kind of risk in the right way.

Let’s shift from “what to avoid” to “what to do instead.” These principles are simple, boring, and deeply effective when you stick to them.

Principle 1: Protect the Downside First

Most people start by asking, “How much can I make?”

Professionals start with, “How bad could this get, and can I live with that?”

Protecting the downside means:

- Not risking rent or food money on investments

- Having at least a small emergency fund

- Avoiding bets that could wipe you out completely

When your basics are protected, you can take healthy risks without constant panic.

How to apply it:

- Aim for 3–6 months of essential expenses in a simple savings account.

- Don’t invest money you’ll need within the next year or two.

- Say no to any opportunity that could ruin you if it goes wrong.

Principle 2: Match Risk to Time Horizon

Your timeline matters more than most beginners realise.

- Money you need soon (0–2 years) should be kept very safe.

- Money for medium-term goals (3–7 years) can handle some ups and downs.

- Money for long-term goals (10+ years) can be in growth assets with more volatility.

The problem comes when people mix this up—like putting their entire house deposit into a volatile asset hoping for a quick gain.

How to apply it:

- List your goals and roughly when you’ll need the money.

- For each goal, decide on a risk level that matches the timeline.

- Revisit this once or twice a year to see if your allocations still make sense.

Principle 3: Focus on Cash Flow and Skills, Not Just Investments

Investments matter, but for beginners, your earning power and cash flow often matter even more.

A reliable way to reduce financial stress is to:

- Build valuable skills

- Increase your income

- Create small, repeatable ways to earn (like freelancing or digital products)

These cash flows give you more money to invest and more resilience when things go wrong.

Tools like WordPress or Notion can help you set up a simple portfolio, blog, or system to manage your projects and clients as you grow.

How to apply it:

- Ask: “What problem can I solve for others that they’d pay for?”

- Start a tiny service-based offer first (easier to validate than product ideas).

- Use extra income to strengthen your safety net and investment plan.

Principle 4: Keep Things Simple and Low-Cost

Complex, high-fee products often benefit the provider more than the customer. Meanwhile, simple, low-cost approaches quietly build wealth over time.

Examples of simplicity:

- Broad, low-fee index funds

- Clear budget and expense tracking

- Straightforward insurance for big risks

You don’t get extra points for complexity. You get extra points for systems you actually understand and stick to.

How to apply it:

- Before buying any financial product, ask, “What are the total fees, and who gets them?”

- Prefer low-fee options and transparent structures.

- If a strategy or product sounds too complicated to explain, skip it for now.

Principle 5: Start Small, Test, and Learn Cheaply

You don’t need to be right about everything. You just need to keep your mistakes small and your lessons big.

Instead of putting a lot of money into every new idea, treat each one as an experiment:

- Invest a small amount first

- Watch how it behaves in different conditions

- Adjust based on what you learn

This applies to investments, side hustles, tools, and even courses.

How to apply it:

- Define a “learning budget”—an amount you’re comfortable losing while you experiment.

- When you try something new, start within that budget.

- Reflect regularly: What worked? What didn’t? What will you do differently next time?

Principle 6: Use Written Rules to Protect Yourself from Your Own Emotions

Money decisions are emotional. Fear, greed, ego, and FOMO can hijack your brain in seconds.

Written rules act like guardrails. They stop you from making huge decisions in heated moments.

Simple rules might be:

- “I never put more than 5% of my net worth into a single asset.”

- “I always sleep on any decision involving more than $X.”

- “I don’t buy anything I don’t understand well enough to explain.”

You can track your rules and notes in a tool like Notion or even a simple spreadsheet. The tool doesn’t matter; the consistency does.

How to apply it:

- Write down 3–5 money rules that match your situation and personality.

- Put them somewhere visible before you log into your bank or brokerage.

- When you feel emotional about a decision, pause and check your rules first.

When you apply these principles, your financial life may still have ups and downs—but they’ll be normal bumps, not cliffs. You’ll know why you’re doing what you’re doing, and you’ll be able to adjust as life changes.

Turning Truth into Action: Practical Ways Beginners Can Start

Reading about principles is nice. But your money situation improves when you do something with them—even if that “something” is small and imperfect.

Here’s how to turn all of this into concrete next steps, based on where you are right now.

If You’re Starting from Zero

Maybe you’re new to money management. Maybe you’ve never invested or feel totally behind. That’s okay. Here’s a gentle starting path:

- Get clear on your numbers.

- Track your income and basic expenses for one month.

- You can do this with a simple spreadsheet or note.

- Build a mini safety buffer.

- Aim for $500–$1,000 set aside for small emergencies.

- Keep it in a basic savings account you can access quickly.

- Learn one simple investment vehicle.

- Read beginner-friendly explanations of broad market index funds or ETFs.

- Your goal is understanding, not action on day one.

- Set a tiny automatic habit.

- For example: transfer a small fixed amount each month into a basic investment account, even if it’s very small.

- Focus on building the habit of consistent investing.

If You’ve Already Started but Feel Messy

Maybe you have some investments, a side hustle, or a bit of crypto, but it all feels chaotic. You’re not sure what’s risky and what’s fine.

- List what you own and what you owe.

- Write down accounts, balances, debts, and interest rates.

- No judgment—this is just your starting map.

- Identify concentration and red flags.

- Is too much of your net worth in one asset or theme?

- Are you in any scheme that triggers multiple red flags from earlier?

- Create a simple risk plan.

- Decide on max % per asset or strategy.

- Decide which holdings are long-term and which are experiments.

- Clean up obvious mistakes.

- Reduce or exit positions that you now see are based on hype, not understanding.

- Redirect that money toward your safety net or clearer investments.

If You’re Recovering from a Bad Experience

Maybe you lost money in a scam, a crash, or a bad trade. That can feel scary and embarrassing—but it can also be a major turning point.

- Acknowledge the loss without self-attack.

- Scams and hype are designed to fool normal people. You’re not uniquely flawed.

- Write a short, honest summary of what happened and what you learned.

- Stabilise before trying again.

- Focus first on rebuilding a basic emergency fund.

- Avoid revenge-trading or “making it back quickly” plans.

- Rebuild with smaller, safer steps.

- Use the red flags and principles in this article as a checklist.

- Only invest in things you can clearly explain and control.

- Turn your lesson into a rule.

- For example: “I never invest in anything with guaranteed high returns,” or “I always test withdrawals with a small amount first.”

Bit by bit, these actions compound. You become someone who:

- Spots bad deals early

- Uses simple, solid strategies

- Knows how much risk they’re taking and why

You don’t need to be perfect. You just need to be a little bit wiser and more intentional each month. That alone can change your financial trajectory over the next few years.

Realistic Scenarios: From Hype Victim to Informed Action Taker

Sometimes abstract principles feel far away from real life. So let’s bring everything down to earth with a few realistic scenarios.

As you read, try to see pieces of yourself in these characters. The goal isn’t to judge, but to recognise patterns—and see how small changes in thinking and behaviour can completely change the outcome.

Scenario 1: The “Next Big Thing” Chaser

Before: Living on hype and FOMO

Linh is 27, has a decent job, and a bit of savings. Most of her money sits in a bank account “for safety,” but every now and then she gets pulled into the latest “big opportunity.”

One month it’s a coin that “everyone in the group chat” is buying.

Another month it’s a new platform promising big daily returns through some “smart” system.

Her typical pattern looks like this:

- Sees screenshots of crazy gains in a Telegram group or on social media

- Feels like she’s missing out and “being left behind”

- Reads just enough to feel it’s real, then throws in a few hundred dollars

- Watches the price obsessively

- Panics and sells low when things fall, or gets stuck when withdrawals are “temporarily disabled”

Over a couple of years, she’s cycled through multiple hypes. Sometimes she doubles her money, sometimes she loses half. Overall, she’s stressed, confused, and not much further ahead.

The turning point

One day, after yet another “guaranteed” platform suddenly shuts down, Linh realises she’s tired of bouncing between fear and greed. She decides: “I don’t want to live like this. I want a plan, not just vibes.”

She starts learning the basics of risk instead of just looking at potential returns.

After: Using risk thinking like a filter

Linh applies some simple changes:

- She makes a short list of red flags she will not ignore again: “guaranteed high returns,” “unclear how money is made,” “hard to withdraw.”

- She separates her money into buckets:

- Essentials and emergency fund

- Long-term investments

- A small “experiment” bucket for things she’s curious about

- Before putting money into anything, she asks:

- “Can I explain how this works to a friend?”

- “What could go wrong?”

- “If this goes to zero, will it destroy my life?”

Now, instead of throwing her whole savings into the newest platform, she might put a tiny amount into something speculative, but only after she’s built a solid base in simple, diversified investments.

Money result

Linh still experiments sometimes, but the experiments are small. The core of her money is no longer driven by hype. Over a few years, her net worth grows more steadily, and the emotional rollercoaster calms down. She feels like the boss of her decisions instead of a passenger.

Scenario 2: The Overconfident “I Know What I’m Doing” Trader

Before: Winning big, losing bigger

Nam has been trading on and off for a couple of years. He has some knowledge, knows how to read charts, and has had a few big wins. The problem is, he’s never really thought deeply about risk.

His habits:

- Uses high leverage “because otherwise the gains are too small”

- Sizes positions based on excitement, not a percentage of his total account

- Doubles down to “make back” losses

- Keeps no real emergency fund, because “my trading account is my backup”

Sometimes, things go really well. He feels smart, powerful, and ahead of everyone else. Then a fast move against his position triggers forced liquidation. Suddenly, months of gains vanish in a day.

The turning point

After a particularly brutal loss that forces him to borrow from friends to cover living expenses, Nam has a sobering moment. It hits him: “If I keep doing this, it’s only a matter of time before I blow up completely.”

He decides to stop trading for a month and reflect on what went wrong—not with the market, but with his behaviour.

After: Trading like a risk manager, not a gambler

Nam comes back with new rules:

- He caps leverage to a very low level or avoids it entirely for a while.

- He never risks more than a small, fixed percentage of his total account on any single idea.

- He separates emergency savings from trading capital. That money is never touched.

- He plans entries, exits, and maximum losses before clicking any button.

He also accepts a hard truth: he doesn’t need to trade constantly. It’s okay to be mostly in simple, long-term investments and only trade a small portion of his capital.

Money result

Nam’s profits are not as spectacular as before, but his losses are much smaller. Over time, his account size grows more steadily instead of yo-yoing. He stops needing to explain sudden disasters to friends and family. Most importantly, he keeps himself in the game long enough for skill and discipline to pay off.

Scenario 3: The Quiet Saver Who’s Afraid to Invest

Before: Safe, but slowly falling behind

Lan is careful, organised, and hates the feeling of losing money. She grew up seeing relatives lose savings in bad investments, so she made herself a promise: “That will never be me.”

Her strategy:

- Keep almost everything in a savings account

- Maybe buy a tiny bit of gold or something similar “just in case”

- Reject any idea that sounds like “investing” as too risky

She sleeps well at night, but there’s a hidden problem: prices keep rising. Rent goes up, food goes up, everything goes up. Her salary increases slowly, but her savings don’t grow much at all.

She starts to notice that despite years of “being safe,” she doesn’t feel more financially secure. In fact, big future goals like a house or retirement feel further away.

The turning point

Lan reads about inflation and realises that doing nothing is not as safe as it seems. She starts to see that there are different types of risk, and that hiding from one kind (market risk) has pushed her into another (inflation and opportunity risk).

She doesn’t want to gamble. She just wants a path that gives her a fair chance.

After: Building a calm, long-term plan

Lan decides to:

- Keep her emergency fund in cash, so she still feels safe about everyday surprises

- Take a small portion of her savings and invest it in simple, diversified funds

- Learn the basics of long-term investing and compound growth

She starts very small, just to get used to seeing her balance move up and down. As she builds confidence, she slowly increases her monthly contributions.

Money result

Nothing dramatic happens in month one or two. But over a few years, Lan sees her investments grow. Some years are down, most years are up. Overall, she’s clearly ahead compared to keeping everything in cash.

Her mindset shifts from “Investing is gambling” to “Investing is a tool. If I use it carefully, it helps me.” For the first time, long-term goals feel possible, not just hopeful.

Optional FAQ (for Leftover Doubts)

Even after you understand the myths, red flags, and principles, it’s normal to have lingering questions. Let’s address some of the most common ones beginners have about risk and money.

“Is It Too Late for Me to Start Managing Risk Properly?”

Short answer: no.

Whether you’re 20, 40, or 60, the best time to start making better decisions is now. You can’t change past choices, but you can stop repeating the same patterns.

What changes with age is:

- Your time horizon (how long your money can stay invested)

- How aggressive your investments should be

- What you’re optimising for (growth vs stability vs income)

If you’re younger, you can typically take more market risk with a portion of your money, because you have time to recover from downturns. If you’re older, you’ll lean more toward capital protection—but even then, keeping everything in cash can still be risky over a long retirement.

The key is to:

- Protect your near-term needs (next few years)

- Use appropriate risk for your longer-term goals

- Avoid big, unnecessary risks that could derail your plans completely

It’s not about perfect timing. It’s about building a smarter structure for your money from this point forward.

“How Do I Know If I’m Being Too Conservative or Too Aggressive?”

A simple way to think about it:

- If market dips make you unable to sleep or function, you’re probably too aggressive.

- If your money feels “safe” but your future goals (house, retirement, freedom) all feel impossible, you might be too conservative.

Ask yourself:

- “If my investments dropped 20–30% on paper, what would I do?”

- “If my savings grew only slightly above inflation for the next 10–20 years, how would that affect my goals?”

Your answers will guide you. You can then adjust by:

- Changing how much you keep in safe assets vs growth assets

- Increasing or decreasing your monthly investing amount

- Gradually stepping your risk up or down instead of making huge shifts overnight

It’s okay to treat this as an ongoing experiment, especially in your first few years.

“Do I Need a Financial Advisor, or Can I Do This Alone?”

You can learn to manage basic risk and investing yourself. The core ideas are not rocket science.

However, a good advisor can help if:

- Your situation is complex (multiple incomes, businesses, inheritance, etc.)

- You’re prone to emotional decisions and want someone to keep you grounded

- You simply don’t have the time or interest to manage everything yourself

If you choose to work with an advisor:

- Make sure you understand how they get paid

- Avoid anyone who pushes complex, high-fee products you don’t understand

- Remember that an advisor is a guide, not a dictator—you still need to understand the big picture

If you decide to go solo, keep it simple:

- Use straightforward products

- Follow clear, written rules

- Learn gradually instead of chasing advanced strategies immediately

“Can I Still Take Big Swings Sometimes?”

Yes—but they should be controlled swings, not life-or-death gambles.

If you have:

- An emergency fund

- Basic insurance

- A solid, boring core investment plan

…then it can be reasonable to allocate a small, clearly defined portion of your money to higher-risk ideas you believe in.

The key is to:

- Set a limit (for example, 5–10% of your investable money)

- Accept you could lose most or all of that portion

- Avoid increasing your bet just because of excitement or peer pressure

This way, you can still participate in exciting opportunities without putting your entire financial life on the line.

“What If I Make a Huge Mistake Again?”

You will make mistakes. Everyone does.

The goal is not to avoid all mistakes forever. The goal is to:

- Make mistakes with small amounts

- Learn from them instead of hiding from them

- Use those lessons to upgrade your rules and systems

If you mess up:

- Be honest with yourself about what happened

- Identify which myth or red flag you ignored

- Turn that into a new rule so it’s much harder to repeat next time

Over time, your mistakes become tuition—a cost you pay once to gain wisdom you keep forever.

Key Lessons & Takeaways

Let’s bring everything together into a handful of clear points you can carry with you.

- Risk never disappears—it just changes shape.

Keeping everything in cash feels safe but exposes you to inflation and missed opportunities. Going all-in on hype exposes you to big, fast losses. Smart money choices come from recognising which risk you’re taking and choosing it on purpose. - If returns sound magical, the risk is being hidden from you.

“Guaranteed” or “risk-free” high returns, vague explanations, and heavy pressure are giant red flags. Saying no to these offers is one of the fastest ways to protect your savings and emotional energy. - Simple, boring systems tend to win over time.

A basic emergency fund, sensible insurance, and regular contributions to transparent, low-complexity investments often beat complex products and constant “opportunities.” Boring is not the enemy—confusion is. - Your behaviour matters more than any single investment.

Chasing trends, reacting emotionally, and ignoring your own rules can destroy even a good portfolio. Thinking ahead, starting small, and being consistent can rescue even an imperfect plan. - You don’t have to be fearless—you just have to be intentional.

You can still be cautious, sceptical, and careful while using risk as a tool to build the life you want. The shift is from “I hope this works” to “I know what I’m risking, why I’m risking it, and how I’ll respond if it goes badly.” - Every step you take makes future steps easier.

Tracking your money, building a tiny buffer, testing a small investment, writing your first money rule—each of these is a real, practical move toward being an informed action taker instead of a hype victim.

If you use this article as a checklist—spotting myths in your thinking, catching red flags in offers you see, applying the principles, and taking small, concrete actions—you’ll already be far ahead of most people who are still letting fear or hype drive their decisions.

Your goal isn’t to become a perfect “risk expert.” Your goal is to become the kind of person who treats money decisions with respect, curiosity, and intention. That alone can change your financial story over the next few years much more than any “secret” strategy ever will.

Disclaimer

The information in this article is for educational and general informational purposes only. It is not financial advice, investment advice, legal advice, tax advice, or any other professional advice.

Financial decisions always involve risk, and your personal situation, goals, risk tolerance, and local regulations may be very different from the examples used here. Do not make, change, or stop any investment, business, or financial decision based solely on this content.

Before acting on any idea or strategy mentioned in this article, you should:

- Do your own research

- Carefully assess your own financial situation

- Consider speaking with a qualified professional (such as a licensed financial advisor, accountant, or lawyer) in your country or region

The author and publisher do not guarantee any specific results or outcomes and are not responsible for any losses, damages, or consequences that may arise from using or relying on the information in this article. You are fully responsible for your own money decisions.

☕ Enjoyed this guide?

If my work helped you see money and risk more clearly, you can buy me a coffee to support more practical, beginner-friendly content. Your support means a lot! 💛

👉 https://timnao.link/coffee

{kind=link}