🌍 Smarter Money Ahead: Why Programmable Finance Is a Game-Changer 🚀

Programmable finance is more than just a buzzword—it’s quickly becoming the backbone of how money will move, grow, and even “think” in the years ahead. If you’ve ever wondered why sending money abroad costs so much, why freelancers wait days to get paid, or why investing in real estate feels out of reach, programmable finance has the answers.

Unlike traditional systems that rely on slow banks and costly middlemen, this new wave of digital money is built on blockchain, smart contracts, and tokenization. That might sound technical at first, but the truth is simple: programmable finance is about giving you more control, fewer fees, and faster access to opportunities once reserved for the wealthy.

In this guide, we’ll walk through the basics in plain English, show you how programmable finance is already being used in everyday life, and explore where the future of money might be headed. By the end, you’ll not only understand how it works but also see practical steps you can take today to get started safely.

Table of Contents

- 💡 Understanding Programmable Finance in Simple Terms

- 📜 From Barter to Blockchain: The Evolution of Money

- 🔗 How Blockchain and Smart Contracts Make Money “Think”

- 💵 Stablecoins Explained: Digital Dollars for Everyday Use

- 🏠 Tokenized Assets: Owning a Piece of the Future

- 🤖 AI Meets Finance: How Agentic AI Becomes Your Money Assistant

- 🌐 Real-World Use Cases You Can Relate To

- Sending Money Abroad

- Getting Paid as a Freelancer

- Investing in Real Estate or Bonds

- Running a Business with Digital Assets

- 🏛️ Governments and Regulations: Why Rules Matter

- 🚀 Opportunities for Beginners: How to Get Started Safely

- 🔮 What the Future of Money Could Look Like

💡 Understanding Programmable Finance in Simple Terms

Most of us think of money as something simple: cash in our wallet, numbers in a bank account, or balances on a mobile app. But money is now evolving into something much smarter. Instead of just storing value or making payments, it can follow instructions, move automatically, and even make financial decisions on your behalf. This is what experts call programmable finance.

In plain language, programmable finance means money that works according to rules written in code. Think of it like setting up a “smart reminder” on your phone. Just as your phone alarm goes off at the right time without you pressing a button, programmable money can act without you logging in or filling out a form. For example, your rent could be paid automatically when your salary comes in, or your savings could be divided across multiple investments instantly, without you doing the math each month.

This is a major shift from how traditional money works. Today, most financial processes involve banks, intermediaries, or at least a human pressing “confirm.” Programmable finance removes much of this manual effort by using blockchain, smart contracts, and AI. These technologies ensure that the rules are executed exactly as written—no delays, no third-party approvals, and minimal risk of human error.

For beginners, the easiest way to understand this is by comparing it to “automation” in daily life. We already automate many things: emails go to spam folders automatically, apps renew subscriptions without asking, and electricity bills can be paid on auto-debit. Programmable finance takes this same principle but applies it directly to money. The result? Faster payments, fewer fees, and financial services that adapt to your needs in real time.

The benefits are not just for businesses or tech experts. Everyday people can use programmable finance to simplify their lives. Imagine you’re a freelancer: instead of chasing late payments, you set up a contract where funds are automatically released when you deliver work. Or picture a student who saves spare change—programmable money could automatically transfer a few cents from every purchase into a savings account. Small improvements like these add up and create better financial habits.

Of course, new ideas always come with questions. Is it safe? How does it work in practice? The good news is that programmable finance is built on transparent, tamper-proof systems. Every transaction is recorded on a blockchain, meaning it’s visible, verifiable, and cannot be altered. Instead of trusting a middleman like a bank, you’re trusting math, code, and cryptography. For beginners, the technical details may sound intimidating, but the big picture is simple: it’s about making money smarter, faster, and more useful.

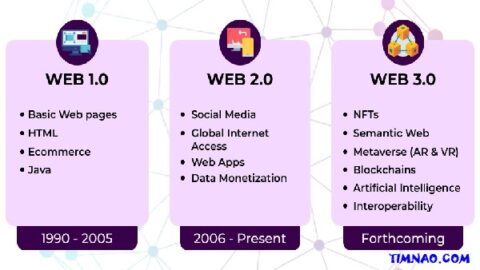

📜 From Barter to Blockchain: The Evolution of Money

To truly appreciate programmable finance, it helps to look back at how money has evolved. Understanding the past makes it clear why we need a new system for the digital age.

The Barter Era: Trading Without Money

In early societies, people exchanged goods directly—grain for cattle, wool for wheat. This was the barter system, and while it worked in small communities, it had a big flaw: you needed a “double coincidence of wants.” If you had wool but wanted rice, you had to find someone who not only had rice but also wanted wool at that exact time. This was inefficient and limited trade.

Commodity Money: Trusting Precious Metals

To fix this, societies turned to commodities like gold, silver, or copper. These had value on their own and were widely accepted. Gold especially became a global standard, trusted as a durable store of value. But carrying and transporting gold was heavy, and supply couldn’t keep up with growing trade. This led to a big breakthrough: paper money.

Paper Money: Value Represented, Not Carried

First introduced in China, paper money allowed people to carry notes that represented the gold stored elsewhere. Later adopted worldwide, this concept transformed trade. It wasn’t the physical gold that mattered anymore but the record of ownership. Fast-forward a few centuries, and banks, central banks, and governments became responsible for issuing and managing this money. This created convenience but also introduced dependence on institutions.

Credit Cards: The Plastic Revolution

In the 20th century, money took another leap. Credit cards replaced cash for everyday spending, enabling global commerce with just a swipe. But behind the scenes, transactions went through multiple layers: banks, processors, and settlement systems. This added speed compared to paper processes but also introduced fees, delays, and dependency on financial institutions.

Fintech and Digital Money

With the internet, apps like PayPal, Stripe, and Venmo emerged. They made sending money as easy as sending a text. However, the infrastructure behind them was still old. Sending $100 abroad could take three days and cost $30 in fees. The systems were digitized but not fundamentally changed.

Bitcoin: The First Decentralized Money

In 2008, during the global financial crisis, Bitcoin appeared. Unlike traditional money, it didn’t rely on banks or governments. It was powered by blockchain, a decentralized ledger where transactions are verified by code, not intermediaries. Bitcoin showed that money could be borderless and independent—but its volatility limited it as everyday currency.

Ethereum and Programmable Finance

In 2015, Ethereum introduced something new: smart contracts. These are codes that can execute agreements automatically. For example, instead of hiring a lawyer or banker to handle an escrow, a smart contract can do it instantly and transparently. This was the birth of programmable finance—where money is not only digital but intelligent.

Stablecoins: Digital Dollars With Stability

To solve the volatility problem, stablecoins were created. Pegged to the US dollar or other assets, they combine the stability of traditional money with the speed of blockchain. Today, stablecoins like USDC and USDT are used for international transfers, business payments, and even everyday expenses.

Why Blockchain Is Today’s Turning Point

The journey from barter to blockchain shows one clear pattern: money keeps evolving to solve inefficiencies. Programmable finance is not just another step; it’s a leap. Instead of relying on banks, lawyers, or clearinghouses, money itself now follows logic. That means fewer delays, lower costs, and wider access for billions of people worldwide.

For beginners, the key takeaway is this: programmable finance is simply the next stage in the long history of money. Just as paper replaced gold and credit cards replaced cash, programmable money is set to replace many outdated systems we still use today.

🔗 How Blockchain and Smart Contracts Make Money “Think”

When you transfer money through a bank or PayPal, there’s always a middleman. The bank verifies the sender and receiver, updates its database, and sometimes even waits for another bank to confirm before finalizing the payment. That’s why transfers can take hours or even days.

Blockchain changes this completely. At its core, a blockchain is a shared digital ledger—like a giant spreadsheet—that is visible to everyone on the network. Once information is recorded, it cannot be changed. Every participant can see the transactions, which makes the system transparent and nearly impossible to tamper with.

Unlike traditional systems where a bank is the “trusted authority,” blockchain relies on cryptographic proof and a network of computers to validate transactions. This makes money transfers faster, cheaper, and safer.

Smart Contracts: Code That Executes Agreements

If blockchain is the “ledger,” then smart contracts are the brains behind programmable finance. A smart contract is simply a small program stored on a blockchain. It executes automatically when certain conditions are met.

Think of it like a vending machine. You insert money, press a button, and the machine dispenses your snack without needing a cashier. A smart contract works the same way:

- If payment is received, then unlock the digital asset.

- If a delivery is confirmed, then release funds.

- If rent is due, then transfer tokens to the landlord.

Because everything runs on code, there’s no need to rely on trust in a person or company. The rules are baked into the contract and carried out exactly as written.

Real-World Examples Beginners Can Relate To

- Freelance Payments

A graphic designer could use a smart contract that holds funds in escrow until the client approves the final design. Once approved, the contract instantly pays the designer—no invoices, no chasing late payments. - Insurance Claims

Imagine buying flight insurance that pays automatically if your flight is delayed by more than 2 hours. Instead of filing paperwork and waiting weeks, the smart contract checks airline data and triggers payment immediately. - Subscriptions and Bills

Streaming services could set up smart contracts that deduct stablecoins every month. If your wallet balance runs out, the contract cancels the subscription automatically—saving time and reducing disputes.

These examples show that smart contracts are not just for techies—they can simplify tasks we all deal with every day.

Why This Matters for Beginners

Traditional systems are slow, costly, and limited by working hours. Smart contracts make money active instead of passive. They can split payments between multiple parties, manage investments, or even enforce compliance rules automatically.

For beginners, the key takeaway is this: money can now “think” because it follows coded rules. This means fewer delays, fewer fees, and fewer headaches with paperwork.

💵 Stablecoins Explained: Digital Dollars for Everyday Use

If Bitcoin showed the world that money could be decentralized, it also revealed a problem—volatility. The price of Bitcoin can swing by hundreds of dollars in a single day, making it impractical for everyday purchases like groceries or rent.

This is where stablecoins come in.

Stablecoins are cryptocurrencies designed to maintain a stable value, usually pegged to the US dollar or another fiat currency. One stablecoin typically equals one dollar. This stability makes them the bridge between traditional money and programmable finance.

Types of Stablecoins Beginners Should Know

- Fiat-Backed Stablecoins

These are the most common. For every token issued, a dollar is held in reserve by a regulated institution. Examples: USDC (Circle), USDT (Tether).- Pros: Highly trusted, widely used.

- Cons: Requires trust in the issuer to maintain reserves.

- Crypto-Collateralized Stablecoins

Backed by other cryptocurrencies like Ethereum. To issue $100 worth of stablecoins, you might need to deposit $150 worth of crypto as collateral. Example: DAI (by MakerDAO).- Pros: Decentralized, transparent.

- Cons: Complex and affected by crypto market volatility.

- Algorithmic Stablecoins

These use code to balance supply and demand without collateral. Some projects have failed spectacularly (like TerraUSD in 2022).- Pros: Innovative design.

- Cons: Riskier, not recommended for beginners.

Why Stablecoins Are So Useful

Stablecoins combine the best of both worlds: the stability of traditional money and the efficiency of blockchain.

Practical uses include:

- Sending money abroad: A nurse in the US can send USDC to her family in the Philippines in seconds, with fees under $0.10—far cheaper than Western Union.

- Freelancing and gig work: A freelancer in Brazil can get paid instantly by a US client without waiting days for PayPal withdrawals.

- Online shopping: Some merchants accept stablecoins directly, allowing faster settlement and lower transaction fees.

- Savings and yield: Stablecoins can be deposited into decentralized finance (DeFi) platforms to earn interest, often higher than traditional bank accounts.

How Stablecoins Can Help Beginners Build Better Financial Habits

- Budgeting Made Easy

You can set up separate wallets for rent, groceries, and savings. Smart contracts can move stablecoins into each wallet automatically when your salary arrives. - Instant Emergency Transfers

Instead of waiting 2–3 business days for a bank transfer, you could send emergency funds to a friend instantly—even across borders. - Micro-Savings

Platforms like Sablier or Superfluid allow “streaming money,” where savings can trickle into an account every second, instead of waiting until month’s end. This helps beginners develop consistent saving habits.

Safety and Regulation

Like any financial tool, stablecoins come with risks. Some issuers have faced criticism for lack of transparency. That’s why regulators worldwide are creating clearer rules.

- In the US, the FIT21 Act (2025) now requires stablecoin issuers to keep reserves in cash or Treasury bills, undergo audits, and guarantee 1:1 redemption.

- In the EU, MiCA regulation ensures issuers provide clear disclosures and protections.

For beginners, the best practice is to stick with reputable stablecoins like USDC, which are audited and widely accepted.

The Future of Stablecoins

Stablecoins are becoming the new standard of digital money. They are already integrated into platforms like Stripe for online payments and Coinbase Wallet for global transfers. Central banks are even creating their own versions called CBDCs (Central Bank Digital Currencies), such as China’s digital yuan and Europe’s upcoming digital euro.

This trend signals that programmable finance is not just a “crypto experiment” but the future of how money will work globally.

🏠 Tokenized Assets: Owning a Piece of the Future

For most of history, investing in valuable assets like real estate, art, or bonds was limited to the wealthy. If you wanted to buy property, you needed a large down payment. If you wanted to invest in fine art, you needed millions. The barrier to entry was simply too high for everyday people.

Tokenization is changing this. In simple terms, tokenization means turning real-world assets into digital tokens on a blockchain. Each token represents a fraction of ownership. This makes it possible for anyone—not just millionaires—to invest in assets that were previously out of reach.

How Tokenization Works in Practice

Imagine a $1 million apartment in New York. Traditionally, you’d need either a large mortgage or upfront cash to buy it. With tokenization, the apartment could be divided into 1 million tokens, each worth $1. You could buy 1,000 tokens for $1,000 and instantly become a co-owner.

The blockchain keeps track of who owns which tokens. If you want to sell later, you don’t need a lawyer or real estate agent—you can simply trade your tokens on a marketplace.

Real-World Examples of Tokenized Assets

- Real Estate

Platforms like RealT allow investors to buy fractions of rental properties in the US. Owners receive tokenized rent payments in stablecoins, directly to their digital wallets. - Treasury Bills and Bonds

Companies like Ondo Finance tokenize US Treasury bills, allowing investors to earn safe, government-backed returns with as little as $100. - Art and Collectibles

Startups like Masterworks tokenize fine art from Picasso or Banksy, letting people invest in shares of world-class art without needing millions. - Music Royalties

Artists are beginning to tokenize future royalties, so fans can invest directly in their success. For example, owning tokens tied to a musician’s streaming income could mean receiving a share of future earnings.

Why Tokenized Assets Are a Big Deal for Beginners

Tokenization makes investing more affordable, accessible, and liquid. Instead of needing huge capital, beginners can start with small amounts. Instead of waiting weeks to sell property or bonds, you can trade tokens instantly online.

This also allows for better diversification. Instead of putting all your money into one property or one stock, you can spread $500 across real estate, bonds, and even art—all in tokenized form.

Potential Risks to Keep in Mind

While tokenization is exciting, it’s still new. Platforms vary in terms of legal protections, and regulations are still evolving. Beginners should:

- Use reputable platforms with transparent audits.

- Start small, only investing what you can afford to lose.

- Understand that not all tokenized assets are equally liquid—some may take time to sell.

The key takeaway is that tokenization makes ownership democratic. For the first time, beginners can access investments that used to be locked behind gates of wealth and privilege.

🤖 AI Meets Finance: How Agentic AI Becomes Your Money Assistant

While tokenization opens new doors, managing finances can still be overwhelming. This is where AI-powered financial assistants—sometimes called agentic AI—step in.

In simple terms, agentic AI is like having a smart financial manager that works 24/7, never forgets deadlines, and constantly looks for better opportunities.

What Agentic AI Can Do

- Fraud Detection

AI can monitor your transactions in real time and flag suspicious activity faster than banks. If someone tries to drain your wallet, AI can freeze the account instantly. - Smart Payments

Instead of choosing between credit cards, bank transfers, or crypto, AI can automatically pick the cheapest and fastest route for each payment. - Automated Investing

Agentic AI can allocate your money across different assets based on your goals. For example, it could place some funds into tokenized Treasury bills for safety, some into real estate tokens for growth, and keep a portion in stablecoins for daily expenses. - Negotiating Deals

In the near future, AI agents may even negotiate with vendors or service providers. For example, your AI could scan electricity providers and automatically switch you to the cheapest plan.

Everyday Scenarios Beginners Can Relate To

- Budgeting Made Easy

Instead of manually tracking expenses, AI can categorize spending automatically and suggest areas to save. Imagine it telling you: “You spent 20% more on dining this month. Want me to move $50 back into savings?” - Saving for a Goal

If you’re planning a trip or big purchase, AI can set aside small amounts daily. For instance, $3 per day could be automatically saved into a stablecoin wallet, accumulating into $1,000 over the year. - Debt Management

AI can analyze your loans and suggest the fastest way to pay them down. It might recommend making extra payments toward the loan with the highest interest first.

Current Examples of AI in Finance

- Plum and Cleo are AI-powered budgeting apps that help users save automatically.

- Numerai uses AI to crowdsource stock market predictions.

- Fetch.ai develops autonomous agents for DeFi, handling tasks like finding the best yield rates.

These are early signs of how AI is becoming an active financial partner, not just a passive tool.

Benefits for Beginners

Agentic AI levels the playing field. Tasks that once required professional financial advisors are now available at your fingertips. Beginners can:

- Automate savings and investing.

- Reduce risk with smarter fraud detection.

- Gain confidence knowing that money is actively managed, not left idle.

Things to Watch Out For

AI isn’t perfect. It relies on data and can sometimes make mistakes. Beginners should:

- Always review AI recommendations before acting.

- Use AI as an assistant, not a replacement for judgment.

- Protect privacy by only using trusted apps with clear data policies.

The Future: AI + Tokenization

The real magic happens when AI and tokenized assets combine. Imagine an AI agent managing your tokenized portfolio:

- Reinvesting rental income from real estate tokens into government bonds.

- Automatically balancing risk between stablecoins and higher-growth assets.

- Paying bills directly from your investment earnings.

This is where programmable finance becomes truly hands-free—your money not only works for you but is managed intelligently by AI in real time.

🌐 Real-World Use Cases You Can Relate To

Up to this point, programmable finance, blockchain, and tokenized assets may sound futuristic. But these tools are already here, and they’re making a difference in everyday life. The easiest way to understand their power is to look at practical, real-world use cases that beginners can connect with.

Let’s break down how programmable finance is solving problems you may already face today.

💸 Sending Money Abroad

If you’ve ever sent money internationally, you know the pain: high fees, long delays, and unpredictable exchange rates. Traditional services like Western Union or bank wires can take 3–5 business days, and fees often eat up 5–10% of the amount.

With stablecoins like USDC or USDT, sending money abroad works more like sending an email. It’s near-instant, costs just a few cents, and doesn’t depend on bank hours.

Example:

A nurse working in the US wants to send $200 to her family in the Philippines.

- Traditional route: $15 fee, 2–3 days wait.

- Stablecoin route: $0.10 fee, delivered in under a minute.

The family can then convert stablecoins into pesos through local exchanges or even use them directly if the merchant accepts digital dollars.

For beginners, this means you no longer need to be tied to expensive remittance services. With a simple wallet app, you can move money across borders almost instantly.

🎨 Getting Paid as a Freelancer

Freelancers and gig workers often face challenges getting paid. International clients may use PayPal or bank transfers, which charge fees and can take days. In some countries, these platforms don’t even support withdrawals.

Programmable finance solves this by enabling direct payments in stablecoins or crypto through smart contracts. This ensures faster, cheaper, and more reliable payouts.

Example:

A graphic designer in Brazil delivers a logo to a client in Germany. They agree on $500:

- With PayPal: $25 in fees, 3–5 days for funds to arrive.

- With USDC via blockchain: Less than $1 in fees, funds arrive in minutes.

Some platforms are already building this in. For example, Talent Protocol allows freelancers to get paid in stablecoins, while smart contract escrow platforms can hold funds securely until work is complete.

For beginners, this removes the stress of delayed payments and unfair fees. You keep more of your earnings and get paid faster—two things every freelancer values.

🏠 Investing in Real Estate or Bonds

Traditional investing often requires large amounts of money and access to financial institutions. Buying a property might require a six-figure down payment. Investing in government bonds often requires a brokerage account and minimum amounts.

Tokenization breaks down these barriers by letting you buy fractions of assets. This means you can invest with as little as $10 or $100, instead of thousands.

Real Estate Example:

Platforms like RealT allow investors to own fractional shares of US rental properties.

- You could buy $100 worth of tokens representing a Detroit home.

- Each month, you’d receive a share of rental income in stablecoins.

Bond Example:

Through tokenized bonds (like those offered by Ondo Finance), you could invest in US Treasury bills with small amounts. Instead of a $1,000 minimum, you might only need $10 to get started.

For beginners, this means two big advantages:

- Accessibility — You don’t need to be wealthy to access high-quality assets.

- Diversification — You can spread small amounts across multiple assets, reducing risk.

🏢 Running a Business with Digital Assets

Businesses are also finding practical uses for programmable finance. Whether you’re a small shop owner, an online entrepreneur, or running a startup, digital assets can cut costs and open new opportunities.

- Faster Payments from Customers

Instead of waiting for credit card settlements (which can take days), businesses can receive payments instantly in stablecoins. Lower fees mean higher profit margins. - Paying Employees or Contractors

Companies with global teams can pay workers in different countries without dealing with currency conversion headaches. A programmer in India and a marketer in Canada can both be paid in USDC instantly. - Managing Business Expenses

Smart contracts can automatically handle payroll, subscriptions, or supplier payments. Imagine a contract that splits revenue: 50% to suppliers, 30% to marketing, and 20% to the owner—executed instantly every month. - Raising Capital

Tokenization allows startups to raise money by selling tokenized shares or revenue rights. Instead of chasing venture capitalists, entrepreneurs can offer tokens to early supporters worldwide.

Example:

A small coffee shop could issue “coffee tokens” redeemable for drinks. Loyal customers buy these tokens in advance, giving the shop working capital. Customers benefit by locking in discounts, while the shop gets funding without bank loans.

Why These Use Cases Matter for Beginners

It’s easy to see blockchain and programmable finance as “advanced tech.” But these examples show that it’s about solving real problems people face daily:

- Sending money without losing 10% to fees.

- Getting paid on time as a freelancer.

- Investing in assets once reserved for the wealthy.

- Running a business with smoother cash flow.

For beginners, the most important step is to start small. Download a wallet app, experiment with sending $5 to a friend, or buy a tiny fraction of a tokenized bond. The hands-on experience will teach you more than theory ever could.

🔮 What the Future of Money Could Look Like

Money has always evolved—from shells and gold coins to paper cash and credit cards. Today, programmable finance is shaping the next chapter. The question isn’t whether money will change, but how quickly and in what direction.

Everyday Money That Thinks for You

In the near future, money may become intelligent and automated. Instead of you having to remember bills, budgets, or transfers, programmable money could handle everything in real time.

- Rent: Paid automatically on the first of the month through a smart contract.

- Groceries: Your digital wallet could pay directly when you walk out of the store, no checkout line required.

- Savings: A percentage of every incoming payment could flow instantly into a savings or investment account.

For beginners, this means less stress and more time. Your money will “do the work” instead of sitting idle.

A Borderless Financial World

Today, money often gets stuck inside borders. Sending cash abroad is slow and expensive. In the future, stablecoins and tokenized assets could make global payments seamless.

Imagine a world where:

- A student in Kenya pays for an online course in the US using digital dollars.

- A shop in Thailand accepts tokenized bonds as payment.

- You invest $10 in a Paris apartment from your phone in minutes.

For beginners, this opens opportunities that were once only available to international corporations and wealthy investors.

The Role of AI in Future Finance

Artificial intelligence will make finance more personal and adaptive. Instead of using generic advice, your AI assistant will tailor strategies to your unique habits and goals.

- If you overspend, AI could adjust your budget automatically.

- If interest rates rise, AI could shift your savings into higher-yield tokenized bonds.

- If a bill is due, AI could pay it before you even remember.

This future isn’t decades away—it’s already starting. Apps like Cleo, Plum, and Fetch.ai are showing the first steps toward AI-managed finances.

Central Bank Digital Currencies (CBDCs) in Daily Life

CBDCs could become as common as debit cards are today. Governments want to use digital currencies to:

- Distribute benefits instantly.

- Collect taxes automatically.

- Offer cheaper, faster payments for everyone.

For beginners, this means you may soon receive your salary or social benefits directly into a digital wallet rather than a traditional bank account.

Opportunities and Challenges Ahead

Like any big shift, the future of money comes with both promise and challenges.

Opportunities:

- Easier access to investments.

- Faster global payments.

- Smarter financial management through AI.

Challenges:

- Ensuring privacy in a world of traceable money.

- Avoiding scams and unregulated platforms.

- Learning new tools and habits.

The future of money will likely be a hybrid system—combining blockchain, AI, tokenization, and traditional finance. The earlier you start learning, the more comfortable you’ll be when it becomes the norm.

🙋 FAQs: Beginner Questions About Programmable Finance Answered

To make things even clearer, let’s go through some of the most common beginner questions.

1. Do I need a lot of money to get started?

No! One of the biggest benefits of programmable finance is low barriers to entry. You can start with as little as $5–$20 by buying stablecoins or small fractions of tokenized assets.

2. Is this the same as investing in Bitcoin?

Not exactly. Bitcoin is one part of the crypto world. Programmable finance is much broader. It includes stablecoins, smart contracts, tokenized real estate, and AI-powered financial tools. Think of it as the “infrastructure” for the future of money, not just one asset.

3. Are stablecoins safe?

Stablecoins are generally more stable than cryptocurrencies like Bitcoin because they’re pegged to the dollar. However, safety depends on the issuer. Stick with reputable ones like USDC, which publish regular audits. Avoid risky algorithmic stablecoins.

4. What’s the easiest first step for a beginner?

Download a trusted wallet like Coinbase Wallet or Trust Wallet. Buy a small amount of stablecoins (like $20 in USDC) and try sending it to a friend. This simple experiment will give you real hands-on experience.

5. How do I avoid scams?

- Never invest in projects promising “guaranteed returns.”

- Use platforms with licenses, audits, and a clear track record.

- Double-check website URLs to avoid fake lookalikes.

- Remember the golden rule: If it sounds too good to be true, it probably is.

6. Will this replace banks completely?

Not likely—at least not anytime soon. Banks will probably adapt by integrating blockchain and AI into their services. For beginners, think of programmable finance as an upgrade to the financial system, not a total replacement.

7. What skills should I learn to stay ahead?

You don’t need to be a coder. Focus on:

- Understanding digital wallets and stablecoins.

- Learning basic security practices like managing private keys.

- Exploring beginner platforms for tokenized investing.

With time, you’ll naturally build confidence and grow into more advanced areas.

8. Why should I care if I already have a bank account?

Because programmable finance offers what banks often don’t:

- Lower fees.

- Faster payments.

- Access to global investments.

Even if you’re happy with your bank now, learning these tools prepares you for where money is headed.

9. Can I lose everything if I make a mistake?

If you lose your private keys or fall for a scam, yes, you could lose your funds. That’s why it’s important to start small, use secure apps, and practice safe habits. Over time, you’ll learn to manage risk confidently.

10. How soon will all this become mainstream?

It’s already happening. Big companies like Visa, Stripe, and PayPal are integrating stablecoins. Governments are piloting CBDCs. Experts predict that within 5–10 years, programmable finance will be as common as using mobile banking apps today.

👉 What Beginners Should Keep in Mind

Programmable finance may sound advanced, but at its heart, it’s about making money simpler, faster, and smarter. The future of money isn’t just for techies—it’s for anyone who wants more control over their financial life.

Start small, stay curious, and embrace the change. You don’t need to master everything at once. Even tiny steps today will prepare you for a future where money truly works for you.

⚠️ Disclaimer

This article is provided for educational and informational purposes only. It is not financial advice, investment advice, or legal advice. The concepts of blockchain, programmable finance, tokenized assets, and stablecoins involve risks, and outcomes may vary depending on personal circumstances and market conditions.

Readers should do their own research (DYOR) and, if necessary, consult with a qualified financial advisor, accountant, or legal professional before making any decisions related to digital assets, investments, or financial planning.

The author and publisher of this content make no guarantees of accuracy, completeness, or future performance and are not responsible for any losses or damages resulting from the use of information in this article.

By reading this content, you acknowledge and agree that you are solely responsible for how you choose to use the information provided.

{kind=link}

Of course, what a magnificent blog and informative posts, I will bookmark your blog.Have an awsome day!