Spend Money Wisely with a Calm, Powerful Mindful Spending System 💡

Spend money wisely doesn’t mean cutting all your fun—it means buying in a way that gives you more peace, more options, and fewer “why did I do that?” moments. If you’ve ever treated yourself after a stressful week and then felt that quiet money-stress on Monday, this is for you. In this guide, you’ll learn mindful spending and conscious spending using simple tests and real-world rules you can apply today—so your money supports your life (not your image).

The “small treat” that quietly rewired her whole month

Maya’s “small treat” wasn’t ridiculous.

It wasn’t a designer bag or a luxury vacation. It was the upgraded version of normal life: a nicer dinner, a newer gadget, a better-looking outfit. The kind of purchase you can justify with one sentence:

“I’ve had a long week. I deserve it.”

And honestly? She did deserve nice things. The problem wasn’t the treat.

The problem was what happened next.

The pattern that kept repeating

Here’s how her month usually went:

- Week 1: bills paid, mood okay

- Week 2: stress builds (work, family, life)

- Friday: a “small treat” to feel better fast

- Monday: a quiet pinch—less cash, more anxiety

- Rest of month: “I’ll be stricter later” (but later never really comes)

Nothing exploded. No big crisis. Just a slow leak.

The tricky part is that slow leaks don’t feel like danger. They feel like “life.”

But over time, those little upgrades quietly rewire your expectations. You don’t just buy the nicer dinner once—you start believing that’s the new normal. And when the new normal rises, your stress rises with it.

That’s what happened to Maya: her baseline got more expensive.

The turning point wasn’t guilt—it was a question

One Monday, she opened her banking app and didn’t feel shame. She felt confusion.

She wasn’t shopping every day. She wasn’t “bad with money.” So why did she feel like she was always catching up?

Then she asked a question that changed how she spent:

“Did this purchase make my life better… or did it just make my weekend feel better?”

That’s the doorway into mindful spending.

Because a lot of “treat spending” isn’t about the thing. It’s about the feeling:

- relief

- control

- proof that you’re doing okay

- a momentary break from pressure

If you don’t notice the feeling, you keep trying to solve emotional discomfort with financial decisions. And money is a terrible therapist.

The first “money win” she noticed

Maya didn’t start with a complex budget.

She started with one small rule:

No upgrades on stressed days.

Not “no spending.” Just no upgrades.

If she was stressed and wanted to buy something, she could still buy:

- groceries

- essentials

- something genuinely useful

But she paused anything that was clearly “because I’m stressed.”

Within two weeks, she noticed a real outcome:

- fewer impulse purchases

- fewer Monday regrets

- more money left over without “trying harder”

That’s the weird truth: when your spending becomes intentional, you often save money without feeling like you’re sacrificing.

And that sets up the bigger realization she had next—because the treats weren’t the only issue.

Why “trying to look fine” is one of the most expensive habits

Maya didn’t think she was trying to impress anyone.

She wasn’t posting flashy hauls. She wasn’t bragging. She wasn’t even chasing luxury.

But she was quietly spending to maintain an image: the image of being “fine.”

Fine as in:

- not behind

- not struggling

- not less successful than the people around her

- not the one wearing the older model or skipping the trendy place

This is what makes it expensive: it rarely feels like vanity. It feels like belonging.

The “fine tax” (the money you don’t notice paying)

Trying to look fine has a cost that doesn’t show up as one big purchase. It shows up as a thousand tiny ones:

- paying extra for the “safer” option so nobody questions you

- upgrading because you don’t want to feel left out

- saying yes to plans you can afford, but shouldn’t repeat weekly

- buying the version that signals “I’m doing well” instead of the version you actually need

It’s a tax because it’s not about what the item does.

It’s about what the item says.

And when spending becomes language, it gets emotional. Emotional spending is fast spending.

External life vs internal life (a beginner-friendly way to see it)

Here’s a simple distinction that helps:

- External life: how your life looks to other people

- Internal life: how your life feels to you on an average Tuesday

Conscious spending prioritizes internal life.

Because if your internal life is calm—sleep, health, relationships, time, stability—you don’t need as many purchases to “fix” how you feel.

But if your internal life is stressful, you’ll keep buying quick relief.

A quick exercise: spot your “trying to look fine” categories

If you want to identify where this habit is hiding, do this:

Pick one category and ask, “Would I buy this if I lived alone on a quiet island?”

Common “fine” categories:

- clothes and accessories

- dining and social plans

- tech upgrades

- car and commuting choices

- home decor that’s more for guests than you

- subscriptions that are “standard” in your circle

You don’t need to judge the category. You just need to notice the motive.

The identity trap: “Now I have to keep this up”

The sneakiest part of trying to look fine is what happens after the purchase.

Your brain doesn’t just think:

“I bought a nicer thing.”

It thinks:

“This is who I am now.”

And once it becomes identity, it becomes maintenance.

That’s how lifestyle creep works. Not because you’re weak. Because humans are consistent creatures. We adapt quickly, and we hate feeling like we’re moving backward.

So the real cost isn’t the purchase.

The real cost is the future pressure it creates:

- “I can’t go back to the cheaper option now.”

- “People will notice.”

- “It will feel embarrassing.”

- “I’ll feel like I’m failing.”

That pressure is exactly why mindful spending matters. It helps you buy things that make your life better—without accidentally buying a new standard you can’t comfortably sustain.

One mindset shift that helps immediately

Maya replaced one sentence in her head:

Old sentence: “Can I afford this?”

New sentence: “Can I afford this again and again without stress?”

Because many people can afford a purchase once.

The problem is repetition.

A lifestyle isn’t built from one decision. It’s built from what you repeat.

This one shift made her spending calmer because it forced her to think in patterns, not moments.

And once she saw patterns, she was ready for the most practical tool in this whole system: a way to separate good spending from “expensive emotions.”

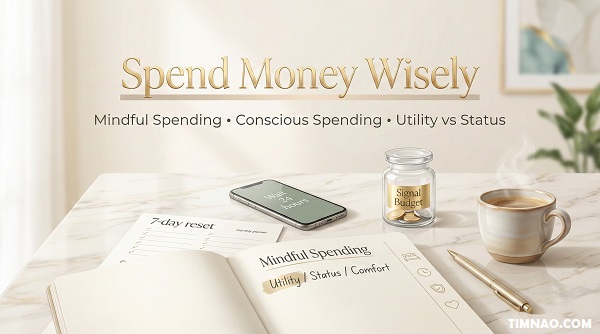

Mindful spending: utility vs status (the Island Test)

If you want a simple way to spend money wisely without turning your life into a spreadsheet, start here:

Utility = a purchase that improves your life in a real, repeatable way.

Status = a purchase that improves how you think you look (or how you hope you’ll be seen).

Status isn’t automatically evil. But it’s dangerous when it’s automatic—because it can quietly drain your budget while giving you very little lasting return.

The goal of mindful spending is not “never buy status.”

The goal is: know what you’re buying and why.

A 10-second self-check before you buy

Before any non-essential purchase, ask these three questions:

- If nobody could see this, would I still want it?

- What problem does this solve next week?

- Will I still be happy I bought this in 30 days?

If the answers are clear and grounded, it’s probably utility (or at least a thoughtful choice).

If the answers feel fuzzy—“I just want it,” “it’s cool,” “everyone has it”—you’re probably in status territory.

The Island Test (the clearest version)

Imagine you live on an island:

- no coworkers

- no social media

- no “keeping up”

- no judgment

You can still have nice things. But you can’t impress anyone.

What would you still pay for?

That list is your utility compass.

Utility examples that actually pay you back

Utility spending often looks boring from the outside—which is why it’s so powerful.

It tends to pay you back in:

- time saved

- stress reduced

- health improved

- work performance boosted

- money saved later

Here are beginner-friendly utility examples (with the “why” attached):

- Sleep upgrades (pillow, curtains, consistent routine tools)

- Why it pays back: better sleep improves mood, focus, and impulse control—yes, even spending decisions.

- Food systems (simple meal prep tools, grocery planning, basic cooking skills)

- Why it pays back: fewer emergency takeout decisions.

- Comfortable daily shoes

- Why it pays back: less pain, longer lifespan, fewer replacements.

- Work tools that reduce friction (a proper chair, second monitor, noise reduction)

- Why it pays back: more productivity, less burnout-driven spending.

- Skill-building (a course, a book, practice tools)

- Why it pays back: increases earning potential or deal quality over time.

A simple way to identify utility is this:

If you use it weekly, it’s a candidate. If you use it rarely, be cautious.

Status spending (not “bad”, just expensive if automatic)

Status spending is often about signaling:

- taste

- success

- trend awareness

- belonging

- “I’m not behind”

And it’s not always obvious. Status spending can show up as:

- buying the logo-heavy version of something

- upgrading early even though the current one works

- choosing the “fancier” plan so you don’t feel cheap

- ordering more than you want because you don’t want to look “basic”

Here’s the key beginner insight:

Status purchases tend to deliver their reward immediately… and then fade.

The item doesn’t necessarily become useless. But the emotional “hit” doesn’t last.

That fading reward is why status can become repetitive:

- you don’t feel the high anymore

- so you need another upgrade

- and another

- until the baseline rises and you feel trapped

A practical way to balance utility and status (without becoming extreme)

You don’t need to eliminate status to be mindful.

You just need to stop letting status make your decisions for you.

Try this simple balance rule:

- Default to utility.

- Schedule status.

Meaning:

- most purchases should improve your real life

- status spending should be planned (so it doesn’t eat your freedom)

If you want a concrete method: make a tiny “status allowance” that you can spend guilt-free. When it’s gone, status waits.

That turns status spending into a choice, not a reflex.

The biggest win: you stop negotiating with yourself

When Maya started using the Island Test, something unexpected happened.

She stopped arguing with herself after purchases.

You know the argument:

- “It’s fine, I deserve it.”

- “I shouldn’t have done that.”

- “I’ll fix it next month.”

- “Why am I like this?”

That mental noise is exhausting—and it often leads to more spending, because stress wants relief.

Mindful spending reduces that noise because the decision is cleaner:

- “This is utility; it supports my life.”

- “This is status; I’m choosing it intentionally (or I’m delaying it).”

And once your decisions become cleaner, your money starts doing what it’s supposed to do: support your life instead of narrating your insecurities.

Now that the “why” is clear, the next step is building a system that keeps this easy—so you can spend money wisely without feeling deprived and without needing willpower every day.

How to spend money wisely without feeling deprived

If you’ve ever tried to “be good with money” by cutting everything, you already know how this story goes.

You last a week. Maybe two.

Then one stressful day hits, and you snap back—often harder than before—because deprivation builds pressure, and pressure eventually demands release.

Maya learned this the frustrating way. She didn’t fail because she lacked discipline. She failed because her plan was built on willpower, not design.

So she made one simple shift:

Instead of “spend less,” she aimed to “spend better.”

That’s the whole point of mindful spending. You’re not trying to remove joy. You’re trying to remove regret.

Upgrade what you touch daily

When people hear “spend money wisely,” they often imagine cutting small pleasures. But the smarter move is usually the opposite:

Spend on the things you interact with constantly—because they quietly shape your mood and your decisions.

Think of it like upgrading the road you drive on every day instead of buying a fancy car you drive once a month.

Here are “touch daily” categories that often give the best return:

- Sleep: pillow, sheets, blackout curtains, a consistent wind-down routine

- Food: basic meal-prep tools, groceries that make weekday cooking easier

- Work: chair support, keyboard/mouse comfort, a setup that reduces friction

- Commute: shoes, bag, earbuds, anything that reduces daily stress

- Home basics: lighting, organization, a few simple tools that prevent chaos

A beginner-friendly rule:

If it improves your life 5+ times per week, it can be worth paying more once.

Because the return isn’t just “quality.” It’s reduced stress and fewer impulse purchases later.

Micro-action (10 minutes)

Make a quick list:

- Write 5 items you use every day.

- Circle the one that causes mild annoyance (pain, mess, wasted time, frustration).

- Pick one small upgrade that solves that exact problem.

Your first win isn’t “being frugal.” Your first win is removing friction, so you stop spending money to soothe irritation.

Stop buying “proof”

This is the one that quietly changes your finances.

“Proof spending” is when you buy something not because it helps your real life, but because it helps you feel like you’re doing okay.

Proof spending often sounds like:

- “I need to look professional.”

- “It’s important for my image.”

- “People will notice if I don’t.”

- “I don’t want to seem cheap.”

Sometimes image does matter (client-facing work, certain industries). The mistake is using image as an automatic excuse.

Here’s how Maya drew a clean line:

She separated “professional utility” from “social proof.”

- Professional utility: helps you do your job, get clients, communicate clearly

- Social proof: signals status to people who aren’t paying your bills

A simple decision rule for beginners:

If it doesn’t help you earn, save, or live better, it’s probably proof.

Not always—but it’s a strong filter.

Micro-action (15 minutes)

Pick one area where you spend for image (clothes, tech, dining, car, home decor). Then do this:

- List the last 3 purchases in that category.

- For each, answer: “What did this help me do?”

- If the answer is mostly “feel seen,” mark it as proof.

Then pick one proof purchase to pause for 30 days. Not forever. Just long enough to see if you actually miss it.

This pause creates real outcomes:

- more cash left at month-end

- less pressure to keep up

- clearer priorities (you start hearing your own taste again)

Comfort beats dopamine (in real life)

A lot of overspending is “dopamine spending”—buying something new to feel better quickly.

The problem with dopamine is that it fades. Then you need a new hit.

Comfort is different. Comfort is steady.

When Maya stopped chasing “new,” she started asking:

“What purchase would make next week easier?”

That question naturally shifts you toward utility.

Here are examples of comfort spending that often beats dopamine spending:

- groceries for simple meals instead of another food delivery spiral

- a gym class pack that builds energy instead of stress-shopping

- a once-a-month deep clean instead of buying stuff to hide mess

- replacing a small broken home item that annoys you daily

- a basic course that upgrades your skills (and future income)

If you want a grounded way to choose comfort, use this mini-score:

Joy per dollar (JPD)

Ask: “How many times will this improve my day this month?”

- If it improves your life once, it must be really meaningful.

- If it improves your life 20 times, even a small upgrade can be worth it.

Micro-action (2 minutes)

Before your next “treat,” ask:

- “Am I trying to feel better or trying to feel different?”

If it’s “different,” dopamine is driving.

If it’s “better,” comfort might actually be the smarter buy.

A small, human transition:

Once Maya stopped feeling deprived—and started feeling in control—she noticed a new problem that had been running the show the whole time: the goalposts kept moving.

The moving goalpost problem: happiness vs contentment

One reason money feels stressful (even when you’re doing “okay”) is that your expectations can rise quietly in the background.

You don’t decide to want more. You absorb it.

New restaurants. Better clothes. Nicer vacations. Upgrades that used to feel special start feeling normal. And suddenly, “normal life” costs more.

This is the moving goalpost problem:

- what used to be exciting becomes standard

- standard becomes expected

- expected becomes “not enough”

And if your spending follows that curve, it can eat your income increase without you noticing.

The “new normal” problem

Here’s what makes the new normal so tricky: it’s not one purchase. It’s the baseline it creates.

A few examples:

- You upgrade your phone early once… and now doing it regularly feels normal.

- You start grabbing nicer coffee daily… and now skipping it feels like deprivation.

- You move to a higher-spend social circle… and now “simple plans” feel awkward.

- You book one premium trip… and now regular trips feel “less.”

None of these are morally wrong. The issue is when the baseline rises faster than your comfort.

A beginner-friendly way to measure baseline stress is this:

“If I had one average month (no bonus, no extra gigs), would my spending still feel calm?”

If not, your goalposts have moved past your stability.

A practical fix: the “good enough” lane

Maya didn’t try to reverse everything.

She picked one category to keep premium (the one that actually improved her real life), and she chose “good enough” in the rest.

This is conscious spending in practice: not equal cuts everywhere—just clear priorities.

Try this simple lane method:

- Premium lane (1–2 categories): you spend more here intentionally

- Good enough lane (most categories): reliable, simple, not performative

- Pause lane (1 category): you reduce for 30 days to reset your baseline

This prevents the common beginner mistake: cutting everything, then rebounding.

A weekly contentment reset (4 minutes)

Contentment is not a personality trait. It’s a practice.

If you don’t practice it, the internet will practice “wanting” for you.

Here’s the 4-minute reset Maya uses once a week:

- Name one thing that used to feel like a dream and is now normal.

(Your laptop. Your apartment. Your lifestyle. Your freedom.) - Ask: “When did I stop noticing it?”

This is the moment the goalposts moved. - Choose one way to enjoy it on purpose this week.

Not a purchase—an action.- clean it

- use it slowly

- share it with someone

- take a quiet moment to appreciate it

- write one sentence about why it matters

- Pick one desire to delay for 7 days.

You’re not saying “never.” You’re saying “not automatically.”

This reset does something very practical:

- it reduces impulse spending

- it lowers the “need” for constant upgrades

- it makes your existing life feel richer, which makes saving easier

And saving becomes easier because you stop trying to buy happiness every week.

The real-world outcome: better decisions and better deals

When your baseline is calm:

- you can wait for sales

- you’re less vulnerable to urgency marketing

- you can say no to social pressure

- you negotiate better (jobs, clients, rent, contracts) because you’re not desperate

That’s not mindset fluff. That’s how opportunity works: margin creates options.

A natural transition:

Once Maya got her baseline under control, she stopped chasing “looking rich” and started aiming for something more useful—being free. That’s where the next distinction comes in.

Rich vs wealthy: the real flex is control

A lot of people look rich and feel trapped.

They have nice things. They go to nice places. They have the “right” lifestyle.

But behind the scenes, they’re tense:

- one bad month would hurt

- they can’t leave a job they hate

- they take clients they don’t like

- they say yes to obligations because they’re afraid to lose income

Maya realized something that surprised her:

What she really wanted wasn’t more stuff. It was more control.

And control is what “wealth” looks like in real life.

What control actually buys you

When you build even a small buffer, your life changes in quiet ways:

- You can say no to bad deals.

- You can wait instead of rushing.

- You can choose quality over urgency.

- You can invest in skills instead of constantly patching stress.

- You can walk away from a toxic environment.

This is why mindful spending is connected to earning and opportunity-building:

- a calmer baseline gives you room to take smart risks

- smart risks lead to better work, better clients, better long-term outcomes

You don’t need a huge income for this to start. You need a gap between what you earn and what you spend.

The “Would I be okay for 12 months?” question

This is Maya’s favorite question now, because it instantly reveals whether your lifestyle is serving you—or controlling you.

Ask yourself:

“If my income stayed exactly the same for the next 12 months, would my life still feel okay?”

There are three common answers:

- Yes.

Great. You’ve built a stable baseline. Your next goal can be growth without panic. - Mostly, but I’d be stressed.

That’s a baseline tuning problem. Small changes can create big relief. - No. I’d be in trouble.

That’s not a reason for shame. It’s a reason for a plan: lower baseline, build buffer, reduce automatic status spending.

Micro-action (20 minutes): the “Control Gap” check

Do this once and you’ll see your situation clearly:

- Write your monthly take-home income.

- Estimate your non-negotiables (rent, bills, essentials).

- Estimate your repeatable “lifestyle extras” (subscriptions, eating out, rides, shopping, entertainment).

- Calculate your Control Gap:

Control Gap = Income – (Non-negotiables + Lifestyle extras)

Now the important part:

- If your gap is positive, your goal is to protect it and grow it.

- If your gap is zero, your goal is to create a small gap (even 3–5%).

- If your gap is negative, your goal is to reduce baseline first—before chasing new income.

Even a small positive gap changes your behavior. It reduces panic. It increases patience. It improves decision-making.

A beginner-friendly control goal (not extreme)

Maya didn’t aim for “save half my income.”

She aimed for a simple control target:

One month of expenses.

Not immediately. Just as a milestone.

Because one month of buffer creates a very real flex:

- you can breathe

- you can negotiate

- you can avoid bad decisions made under stress

Once she hit that, she noticed something even more interesting: her spending didn’t feel restricted. It felt intentional. Like her money had a job.

And that’s the whole vibe of conscious spending: money stops being reactive and starts being supportive.

A smooth transition to the next section:

With control growing, Maya started noticing a different kind of cost—not on receipts, but in expectations from the world around her. That’s where “social debt” comes in next.

Maya thought the expensive part of “looking successful” was the stuff: the nicer meals, the upgraded phone, the clothes that felt more “put together.”

She didn’t expect the after-cost.

Because once you buy certain things, you don’t just own them—you start managing the expectations that come with them. And that expectation-management has a name:

Social debt.

Social debt is the pressure (spoken or unspoken) to keep spending at a level that matches the identity you’ve shown people. It’s the “maintenance fee” on your lifestyle.

And it’s sneaky because it doesn’t show up as a bill. It shows up as feelings:

- “If I don’t keep up, people will notice.”

- “I can’t go back to the cheaper option now.”

- “I don’t want to look like I’m struggling.”

- “I’ll just say yes this time.”

Over time, those feelings can cost you more than the original purchase.

Social debt rarely arrives with a dramatic moment. It arrives with small, reasonable decisions that stack.

1) The “new default” in your group

You start hanging out in places where spending is the entry ticket:

- dinners where splitting the bill is automatically pricey

- weekend plans that always involve shopping, drinks, or tickets

- friend circles where “treat yourself” is the baseline language

You don’t have to stop seeing people you love. But you do need to notice when the default plan is constantly expensive.

Beginner move: Suggest one “low-cost, high-quality” alternative each week.

- coffee + walk

- potluck dinner

- movie night at home

- free events in your city

If your friendships are real, they’ll survive a cheaper plan.

2) The identity upgrade that becomes a trap

When you upgrade something visible—car, wardrobe, phone, neighborhood—your brain quietly says: “This is me now.”

Then “me now” requires:

- matching accessories

- matching experiences

- matching standards

That’s how one upgrade turns into five.

Beginner move: Before a visible upgrade, write down the full ecosystem it might trigger.

Example: “new laptop” can trigger accessories, software, bags, subscriptions.

If you still want it after seeing the ecosystem, great. If not, you just saved yourself a chain reaction.

3) The fear of looking inconsistent

This is the most expensive one.

People often keep spending not because they love the lifestyle, but because they fear the “step down” feeling:

- “I used to go there… now I can’t?”

- “I used to wear that… now I don’t?”

- “I used to travel like that… now I’m staying home?”

You don’t owe anyone consistency at the cost of your peace.

Beginner move: Practice “confident downsizing language.”

Try one of these simple lines:

- “I’m keeping this month lighter—want to do something simple?”

- “I’m in savings mode right now, but I’m still down to hang out.”

- “I’m focusing on a few priorities, so I’m saying no to extras.”

You’ll be surprised how often people respect clarity.

The quiet compounding advantage

Here’s what Maya noticed after she started reducing social debt: life got quieter—in the best way.

Less pressure to prove. Less urgency to upgrade. Less mental noise.

And that quiet created a powerful compounding effect:

- More margin → more options (better deals, better job choices, less desperation)

- More privacy → less comparison (fewer purchases triggered by envy)

- More consistency → less rebound spending (no “I’ve been good, now I deserve chaos” cycles)

A simple way to remember it:

Social debt makes you fast. Margin makes you patient.

And patience is where smart money decisions live.

Before we move on, one important note: you don’t need to “drop” your lifestyle overnight. You just need a tool that helps you catch social-debt spending before it becomes automatic. That tool is your filter.

Your action system: the Conscious Spending Filter (4 rules)

If budgets make your eyes glaze over, this is for you.

The Conscious Spending Filter is a quick decision tool you can run in under a minute. It’s designed for real life: cravings, stress, social pressure, and the “it’s only $___” temptation.

Use it for any non-essential purchase—especially the ones that feel emotionally urgent.

Rule 1: Delay for clarity

Most impulse spending isn’t a “yes.” It’s a “right now.”

So your first move is not to say no—it’s to create space.

Delay rules that work for beginners:

- Under $50: wait 24 hours

- $50–$200: wait 72 hours

- Over $200: wait 7 days

During the delay, you don’t “ban” the purchase. You just watch what happens to your desire.

Micro-action: Add it to a list called “Later” (not “Never”).

If you like apps, a note in Apple Notes or Google Keep works. If you like simple, use a piece of paper on your desk.

If you still want it after the delay, you’re choosing—not reacting.

Rule 2: Cap status with a “signal budget”

Status spending is not evil. But it is dangerous when it’s unlimited and untracked.

A signal budget is a small monthly amount you’re allowed to spend on “looking good,” “feeling cool,” or “keeping up” guilt-free.

Why this works: it protects your freedom while still letting you enjoy aesthetics and fun.

How to set it (beginner-friendly):

- Pick an amount you can spend without stress (start small).

- Put it in a separate category/account.

- When it’s used up, status spending pauses until next month.

This removes the internal debate. You don’t have to wonder if you’re being “too strict” or “too loose.” The cap decides.

Rule 3: Measure joy per dollar

This rule keeps you from paying a lot for a tiny, short-lived reward.

Ask two questions:

- “How many times will I use/enjoy this in the next 30 days?”

- “Will it make my average Tuesday better?”

That second question is magic because it pulls you out of fantasy spending and back into reality.

Quick scoring (0–2 points each):

- Use it weekly? (0/1/2)

- Reduces stress or saves time? (0/1/2)

- Improves health, sleep, or work? (0/1/2)

- Still valuable in 6 months? (0/1/2)

Total:

- 0–3: likely impulse or status

- 4–6: maybe—delay and rethink

- 7–8: strong utility candidate

No spreadsheet required. You can do it in your head while waiting in line.

Rule 4: Stress rule (buy comfort, not upgrades)

This is the rule that saved Maya the most money.

When you’re stressed, your brain wants fast relief. That’s when you’re most likely to “treat yourself” into regret.

So the stress rule is simple:

If you’re stressed, you can buy comfort—but you pause upgrades.

Comfort purchases are things that calm your nervous system without raising your lifestyle baseline.

Upgrades are things that raise identity expectations.

Examples of comfort (usually safe):

- a simple meal that saves your energy

- a low-cost activity that relaxes you

- a small home fix that removes daily irritation

- a book, a walk, a gym session, an early night

Examples of upgrades (pause them):

- tech upgrades

- visible fashion upgrades

- premium experiences you’d feel pressured to repeat

- “this will make me feel like a new person” purchases

Micro-action: Create a “Comfort Menu” with 10 options on your phone.

When stress hits, you pick from the menu instead of shopping your way out of anxiety.

Once you’ve run the filter a few times, something changes: your spending starts to feel like a skill. And skills are easier when you can see how they fit your specific life. That’s where the practical paths come in.

Practical paths: pick the one that fits your life right now

You don’t need the “perfect” system. You need a system you’ll actually use on a normal week.

Pick the path that matches your situation and run it for 14 days. Your goal is a first measurable win—something you can point to, like “I saved $60,” “I stopped impulse buys,” or “I felt calmer checking my account.”

Beginner with no system (and no patience for budgeting apps)

Your goal: stop mystery spending without tracking everything.

What to do (30 minutes today):

- Open your bank or card transactions.

- Look at the last 10 non-essential purchases.

- Label each one: Utility, Status, or Comfort.

- Circle the top 2 that were clearly “status + stress.”

Next 7 days (simple rules):

- Use the 24-hour delay on anything non-essential.

- Replace one “status + stress” purchase with one item from your Comfort Menu.

First measurable win: 1 week with fewer impulse buys + at least $20–$100 not spent.

If you want a light tool, track just three numbers in Google Sheets:

- non-essential total

- utility wins

- status leaks

That’s enough to see patterns.

Freelancer/creator with uneven income

Your goal: protect your calm on low months and avoid “celebration spending” on high months.

What to do (45 minutes):

- Pick a “Minimum Calm Number” (essentials + basic life).

- Create two buckets:

- Calm Money (minimum calm)

- Flex Money (everything else)

- When you get paid, fund Calm Money first.

Next 14 days (simple rules):

- Use the Conscious Spending Filter on any purchase over a set amount (pick $40 or $50).

- Create a signal budget so success doesn’t turn into lifestyle creep.

First measurable win: you finish the month with money left in Calm Money (even a small amount) instead of starting over at zero.

Small business owner fighting lifestyle creep

Your goal: keep profit from turning into pressure and build a buffer that improves decision quality.

What to do (60 minutes):

- List your “social debt” expenses (things you feel you must maintain to look established).

- Pick one to reduce for 30 days without harming operations.

- Route that saved amount into a buffer account.

Next 14 days (simple rules):

- Run the filter on any “visibility spending” (branding upgrades, hosting, events, gear).

- Ask: “Does this purchase increase revenue, reduce costs, or reduce risk?”

First measurable win: a growing buffer, even if it starts at $25–$100 per week. That buffer buys confidence—and confidence improves deals.

Limited time (1–2 hours/week)

Your goal: spend money wisely by buying back time and reducing decision fatigue.

What to do (1 hour):

- List 5 weekly stress points (mess, food, commuting, admin, sleep).

- Choose 1 utility purchase or service that reduces one stress point.

- Choose 1 status habit to pause for 30 days.

Next 14 days (simple rules):

- Only one “upgrade” per month; everything else must pass the joy-per-dollar test.

- Use the delay rule for anything bought after 9pm (late-night purchases are rarely your wisest ones).

First measurable win: one calmer weekend + fewer “why did I buy that?” moments.

A small note to make this feel human (because it is)

Maya didn’t become a different person. She didn’t stop liking nice things.

She just stopped letting stress and social pressure drive her spending. And that one change gave her something most people want more than a new purchase: breathing room.

Next up in the table of contents is a short reset plan you can run in a week—because once you’ve got the filter and your path, you’ll want a simple “do this next” structure to lock it in.

Mistakes that break mindful spending (and how to avoid them)

Mindful spending sounds simple on paper: pause, think, buy intentionally.

In real life, it breaks for very human reasons—stress, social pressure, and that tiny voice that says, “It’s not even that expensive.”

The good news is you don’t need to be perfect. You just need to recognize the few mistakes that cause 80% of the damage—and put guardrails in place.

Mistake 1: Treating mindful spending like punishment

A lot of people start mindful spending with the energy of a strict diet:

- “No more fun.”

- “I’m cutting everything.”

- “I’ll be disciplined this time.”

That mindset makes your brain feel deprived, which creates pressure, which creates rebound spending.

What it looks like in real life

- You cancel every little joy, then overspend on one “finally I deserve it” day.

- You try to be perfect for 10 days, then feel like you “failed,” so you stop.

How to avoid it

Think of mindful spending as better buying, not less buying.

Try this rule:

Keep one joy category on purpose.

Choose something that genuinely improves your week and fund it without guilt.

Examples:

- one weekly meal out (with a cap)

- a small hobby budget

- one experience that recharges you

Mindful spending sticks when it feels like freedom, not punishment.

Mistake 2: Confusing “cheap” with “wise”

Buying the cheapest option can be smart… or expensive later.

The goal is not cheap. The goal is value.

What it looks like

- You buy a low-quality version, it breaks, you replace it, and you spend more total.

- You buy something uncomfortable or inconvenient, and you keep spending to “fix” the frustration.

How to avoid it

Use a simple beginner filter:

- Will I use this weekly?

- Will it reduce stress, time, or pain?

- Will I still like it in 6 months?

If yes, paying more once can be wiser than paying less repeatedly.

Mistake 3: Not separating “comfort” from “upgrade”

This one is a silent budget killer.

When you’re stressed, your brain wants relief. If you don’t have a plan, you default to upgrades:

- a new outfit

- a new gadget

- a premium treat

- “something that makes me feel like a new person”

But upgrades often raise your baseline, which creates ongoing pressure.

How to avoid it

Follow the stress rule:

- Buy comfort, not upgrades.

Comfort examples:

- simple food that saves energy

- a low-cost calming activity

- a small home fix that removes daily friction

- a book or class that builds you up without raising lifestyle expectations

If you want help making this automatic, keep your Comfort Menu in one place (phone note). If you use Google tools, Google Keep is perfect for this.

Mistake 4: Making decisions while you’re hungry, tired, or emotional

Most “bad spending” isn’t stupidity. It’s biology.

When you’re tired or emotionally overloaded:

- you want fast relief

- you tolerate less friction

- you crave novelty

- you’re more vulnerable to urgency marketing

How to avoid it

Create a simple rule:

- No non-essential purchases after 9pm

(or pick your own time)

If you still want it tomorrow morning, you’ll buy it with a clearer head.

This one rule alone saves a lot of people money because late-night purchases are rarely your wisest ones.

Mistake 5: Tracking everything…then quitting

Beginners often think they need a perfect system.

So they download three apps, categorize every coffee, and burn out within 10 days.

How to avoid it

Track only what helps you make better decisions.

For mindful spending, the simplest tracking that actually works is:

- Status leaks (what you bought to impress or keep up)

- Utility wins (what genuinely improved your week)

- Comfort choices (what helped you relax without escalating your baseline)

If you like simple spreadsheets, track just these 3 numbers weekly in Google Sheets. That’s enough to see patterns without turning your life into accounting.

Mistake 6: Comparing your life to someone else’s highlights

If your spending decisions are constantly triggered by comparison, your “mindful spending” plan won’t survive.

Because comparison creates urgency. And urgency creates purchases.

How to avoid it

Do a 30-day comparison detox:

- unfollow the top 3 accounts that make you feel behind

- unsubscribe from brand emails for a month

- remove one shopping app from your home screen

This isn’t about being anti-social media. It’s about protecting your attention so you can hear your own priorities again.

Mistake 7: Thinking one “good month” means you’re fixed

Mindful spending is a skill. Skills improve with reps.

A good month is great—but the real win is consistency without drama.

How to avoid it

Set one weekly check-in:

- “What was my best money decision this week?”

- “What triggered my worst one?”

- “What will I do differently next week?”

Keep it short. Two minutes. The point is reflection, not perfection.

A natural transition:

Now that you know what breaks mindful spending, let’s lock in a reset that’s actually doable—starting tonight, without a full life overhaul.

A 7-day mindful spending reset you can start tonight

This reset is built for beginners.

No complex budgeting. No “never spend again.” Just a clean plan that creates quick wins and gives you momentum.

Day 1: The 10-purchase reality check (15 minutes)

Open your banking app and pull your last 10 non-essential purchases.

For each, label it:

- Utility (improves life)

- Status (signals image)

- Comfort (reduces stress without escalating lifestyle)

Then answer one question:

Which 1–2 purchases most likely raised my baseline without improving my week?

That’s your first target.

Quick win tonight: Choose one “status leak” to pause for 7 days.

Day 2: Build your “Island List” (10 minutes)

Write 10 things you’d still want if nobody could see your life.

Keep it simple:

- comfort

- health

- time

- calm

- relationships

- a few meaningful experiences

This list becomes your spending compass.

Quick win: Put a star next to the top 3. Those are your priority categories.

Day 3: Create a tiny “signal budget” (10 minutes)

You don’t need to eliminate status spending. You need to stop it from being automatic.

Pick a small number that won’t stress you out (start small). That’s your signal budget for the month.

Rule: If it’s status, it comes from the signal budget. When it’s gone, status waits.

Quick win: Write the amount somewhere visible (note app or paper).

Day 4: Design your Comfort Menu (15 minutes)

Tonight, write 10 comfort options that don’t create lifestyle creep.

Examples:

- walk + music

- home meal + favorite show

- gym session

- tidy one small space

- call a friend

- shower + early night

- library visit

- journal for 5 minutes

Save it in a note so it’s easy to use. If you’re on iPhone, Apple Notes works great.

Quick win: Choose one comfort option you’ll use this week instead of stress-shopping.

Day 5: Add one “delay rule” (5 minutes)

Pick your delay rule and commit for 30 days:

- under $50 → 24 hours

- $50–$200 → 72 hours

- over $200 → 7 days

Quick win: Create a “Later” list. Anything you want goes there first.

You’re not saying no. You’re stopping “right now” from making the decision.

Day 6: Lower one baseline category for 30 days (20 minutes)

Choose one category where your spending has quietly escalated:

- dining out

- online shopping

- subscriptions

- beauty/grooming

- tech upgrades

- “weekend plans”

Then choose a realistic “good enough” version for 30 days.

Examples:

- 1 restaurant meal/week instead of 3

- 1 subscription canceled or paused

- no clothing purchases unless something needs replacement

- one simple home hangout instead of a pricey plan

Quick win: Make the change immediately (cancel, pause, or set your rule).

Day 7: Automate one win (10 minutes)

Automation turns mindful spending from a mood into a system.

Pick one:

- auto-transfer a small amount to savings

- auto-pay a debt amount

- auto-invest (if that fits your situation)

Start tiny if needed. Consistency beats intensity.

Quick win: Set it once, then stop thinking about it.

What you should measure after 7 days (keep it simple)

Choose one measurable result:

- money left over (even $20 counts)

- fewer impulse buys

- fewer “Monday regret” moments

- less stress checking your account

That’s how you know it’s working.

A smooth transition:

If you’ve made it through this reset, you’ve already done the hardest part: you’ve proven you can pause, choose, and spend on purpose. Here are the takeaways to keep it going.

Your Mindful Spending Cheatsheet

- Mindful spending works when it feels like freedom, not punishment. Keep one joy category so you don’t rebound.

- Spend money wisely by protecting your baseline. Ask: “Can I afford this repeatedly without stress?”

- Use the utility vs status lens. Utility improves your week; status signals something—fine occasionally, dangerous when automatic.

- When you’re stressed, buy comfort—not upgrades. A Comfort Menu prevents emotional spending spiral.

- Delay is a superpower. Most “urgent wants” fade after 24–72 hours, and that’s where savings show up.

- Small systems beat big motivation. A signal budget + one automation can change your month without constant effort.

Disclaimer:

This article is for educational and informational purposes only and reflects general personal finance principles. It does not provide financial, legal, tax, or investment advice. Everyone’s situation is different—income, debt, family responsibilities, and risk tolerance can change what “right” looks like. Before making major financial decisions, consider speaking with a qualified professional. Any examples, scenarios, numbers, or outcomes mentioned are illustrative and not guarantees of results.

If this guide helped you spend money wisely and feel more confident with mindful spending, you can support my work by buying me a coffee ☕💛 It keeps the blog going and helps me create more practical, beginner-friendly guides like this.

👉 Buy me a coffee here: https://timnao.link/coffee 🙌✨

{kind=link}